Small Caps Live Weekly Summary

GSK MORE DIS CAPD SDG GATC PRES RFX BOTB RBG CPC PTY SNWS RTN APP

The second part of our Annual Review is now available where we talked about opportunities for 2022. We’ve created a podcast channel to make this easier to access, and may well do more of these interactive recorder chats in the future if this is a format investors like.

Mello Monday is also back next week, with Mark on the twitter panel.

Before diving into our usual stock analysis, it is worth noting that this week we also spotted one of the most ominous chart patterns ever - the vomiting camel:

Here is Vomiting Camel Asset Management’s CIO Katie Martin explaining why it is such a dangerous market signal.

Large Caps Live

GSK (GSK.L) - Consumer Division Demerger/Takeover

The Sunday Times broke the news that Unilever has approached GSK to acquire the consumer goods division that is due to be spun off. I am not entirely convinced that as a standalone business it will command a £50bn - at least until there is a bid. Obviously, the mechanics of the demerger have not been detailed but it will clearly be some kind of distribution to shareholders.

GSK has a market cap of £82.5bn and an EV of £110bn. GSK owns 68% of the consumer healthcare business (Pfizer owns the rest) – so clearly the consumer division – whether it floats at £40bn or £50bn is a significant chunk. At £50bn that would be £34bn to GSK. So I think GSK would pay down some debt, do a special dividend, hold money back for a share buyback and then waste some money on a daft 'transformative' acquisition.

Before we dive into the Consumer business and what it is worth I want to just touch on the US pharma business as I found a fascinating table in the GSK accounts. The following table reflects the difference between the selling price at which GSK sells products and the actual net sales value after it pays rebates and discounts etc:

So basically this table says that it sold £20bn of pharma products in the US but after various rebates/returns and other stuff it really had net sales of £7.45bn. So it is £7.45bn it reports as revenue. I think this table is a fascinating insight into the complications of the US market. Also, note the way the net turnover ‘margin’ has fallen from 41% to 37% over 2 years.

Another point I would make is that everyone thinks that pharma is high-margin. We could restate GSK’s numbers based on the £20bn sales number and put the rebates etc as COGs and then the gross and operating margins would look completely different (though the operating and net profit in £ terms would stay the same).

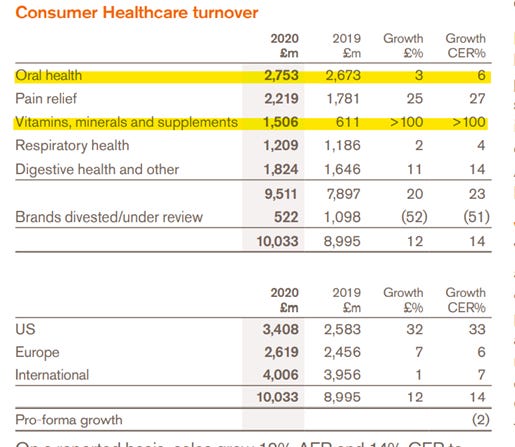

Page 18 of this gives the consumer division’s products. I have always felt that the profitability of the consumer division has been understated. So let’s look at the last accounts – which were in 2020:

So we can see that on a like-for-like basis the consumer healthcare business has not been growing despite the merger with the Pfizer business. Looking at the innovation section of the GSK for the consume business we see breakthroughs such as:

So they are highlighting the launch of Voltaren NSAID gel and also mixing ibuprofen with paracetamol? They don’t sound like particularly groundbreaking consumer products do they?

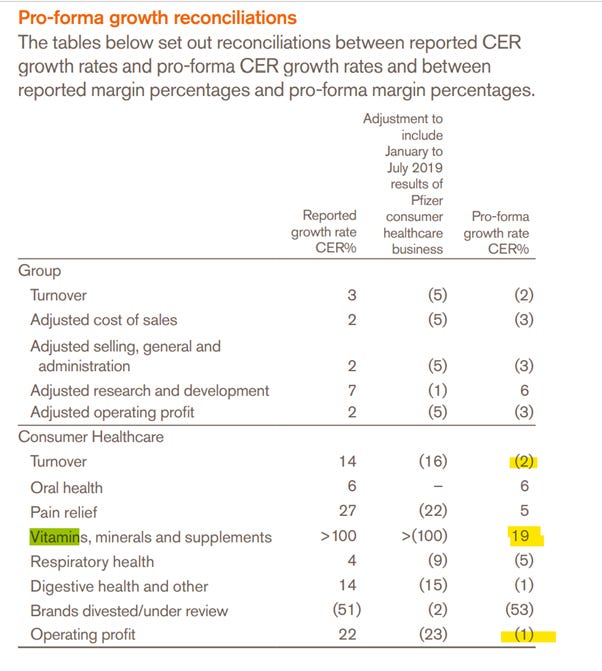

On the oral hygiene side, the company is big in toothpaste (Sensodyne) and other related ie mouthwash. I think the toothpaste market is relatively robust to supermarket brands but I think the mouthwash market is less resistant. (Note that the CER Growth numbers are nonsense due to the acquisition of assets from Pfizer and frankly GSK should not even be publishing numbers like that.)

Digging in, one can see that they are stripping out of the consumer business some costs and losses so I am not entirely convinced that a standalone consumer healthcare business is genuinely as profitable as it appears. I am not entirely sure what the right PAT number for the consumer business is so being generous I get the following:

These are the growth figures:

Regarding vitamins specifically, I would argue that lockdown led to people stuffing vitamins by the lorry load to ensure they did not get Covid. I do wonder how much stockpiling there was and whether it will be sustained. In 2019, the vitamins division had much lower growth.

So what of timelines:

10 Feb Full Year Trading update

28 Feb GSK will give details on its consumer health business

The risk here for Unilever is that:

It overpays

Nestle swoops in and buys the GSK assets

So what happens next:

I think Unilever takes additional credit lines or agrees to performance or deferred payment to reach £55bn for the assets

If GSK holds out for £57 – 60bn then Unilever walks away

Nestle probably runs the slide rule and thinks it can pay £60bn by moving the tax domicile to Switzerland!

Also, there is a chance that Unilever pairs up with private equity or someone like Warren Buffett

Small Caps

Hostmore (MORE.L) - Trading Update

This recent float has gathered some attention since it was a sort of forced sale by private equity and hence the possibility that recent buyers may be getting a bargain.

Mark debated Hostmore as part of a recent Mello BASH, and the thing that made in an “Avoid” for him was the poor reviews on google & trip advisor. An average of around 3.5 stars in his local area was simply not good enough for a chain that is very much at the pricier end of local food options.

This week, they released a trading statement and management also gave an interview to Paul Scott, where a few things stood out to us:

Unbelievably they have to pay 4% of revenue to TGI Fridays in the US for a brand with a potentially negative value that they don't even fully use anymore.

The company themselves refer to it as "the TGI brand". This just underlines what a mess the rebranding business is. Having a restaurant chain branded "Thank Goodness It's Friday" suggests you only go there on Friday. But then calling it "Fridays" with a byline of "Where it's always Friday" which you never actually use and still having everybody still calling it TGIs, including your own management and website URL, seems to raise that bar for insanity.

Management claims that they have fixed the quality issues for the last 8-9 weeks. This seems wishful thinking; it is rare to make a successful culture change in a short period of time. And even if they have it will take a long time for review ratings to trend anywhere near acceptable levels.

Here is the trading statement:

Hostmore plc, the hospitality business focused on American-themed casual dining brand, 'Fridays', and the cocktail-led bar and restaurant brand, '63rd+1st', is pleased to announce a trading update for the financial year ending 2 January 2022.

Further to the introduction of restrictive measures in Scotland and Wales, and the discussions for England to act in a similar manner, the Group is pleased to report that the trading for the month of December 2021 was ahead of early-month expectations.

Revenue for December was 8.3% lower than the comparable period in 2019. Whilst an increased level of guest reservation cancellations became evident as December progressed, and was in line with Government guidance relating to the new Omicron variant, this was more than offset by a combination of new reservations and walk-in demand which reflected the short-term nature of customer decision making while the uncertainty prevailed.

That seems good, but they don’t say if it is like-for-like. They are trialling new restaurants branded “63rd+1st” where, so far, the reviews are very good: Cobham: 4.5, Glasgow 4.0, Harrogate: 3.5 (very new). Cobham used to be a Carluccio’s and is on the high street, unlike a typical TGI Fridays. Anyway, December trading is strong:

Given the strength of December performance, the Board expects EBITDA (pre-IFRS) for the year ending 2 January 2022 to be well ahead of the market consensus of £18.6m.

However, the outperformance appears short-lived:

Trading since 3 January 2022 has been more in line with expectations and reflects what is usually a quieter period post the festive season.

This seems worrying though, given how long they have had to resolve this:

The Group is also continuing its discussions with the remaining landlords on Covid-19 concessions and is optimistic that agreements will be reached in the coming weeks.

The alternative presumably is that landlords send in the bailiffs for non-payment and/or wind the company up?

The replenishment of our balance sheet and the goodwill of our landlord community has enabled the contracting of the latest addition to our estate, being our first QSR store in Dundee, scheduled to open in March 2022. Two further 63rd+1st sites, in Cambridge and Edinburgh, and two Fridays' stores, in Chelmsford and Barnsley, are now scheduled to open in the current calendar year, with more in the pipeline.

It seems daft to be opening new Fridays restaurants when they haven’t got the basics of service and decor sorted, and the brand potentially has a negative value at the moment. They do highlight the cash generation of the business, but statements such as:

Strong cash flow generation is expected to enable the Group to pay down £7.7 million of debt, reducing borrowings 38 % by the end of June 2022.

...must be seen in the context that capex can be deferred for 18 months with little effect, but after that will start causing serious problems. On top of this, Private Equity owners are rarely known for their overinvestment into CAPEX.

Hostmore had a slightly more unusual route to market than the typical Private Equity float. However, the usual warnings about not buying what Private Equity are selling is likely to still apply here.

Distil (DIS.L) - Q3 Trading Update

Before looking into the trading statement, it is worth noting the shifts in spirit trends, with evidence that the gin boom has peaked:

Both whisky and gin have had more than a moment in the spotlight. Now interest is rising in artisan rums, in which provenance and terroir are taken as seriously as they are in wine. One example is the trio of new releases from the Renegade Rum Distillery on the Caribbean island of Grenada. The three sipping rums have been made so that you can taste and appreciate the differences in production methods (column still vs pot still, for instance) and between the varieties of sugar cane (Cane or Lacalome Red here) used to make the spirits.

Distil are not about fine sipping rums. They are about spiced rum for mixing. But they may get some tailwinds from current fashions since By far the most profits come from RedLeg.

The longer-term trend for the Company remains positive, however cumulative (unaudited) revenues for the nine months (April to December 2021) were lapping figures distorted by the initial Covid related lockdowns and consumer stockpiling. Because of its exceptional nature, year on year figures were down 28% versus the same period the previous year, although they were up 23% versus the prior year 'pre-Covid'

Now, this is the sort of thing a company doing badly would say. But, speaking from personal experience, Leo thinks there is at least some element of truth since two things happened to his spirit alcohol purchases when covid started:

He stopped being able to import from abroad / buy duty-free, and

He started stocking up because he'd lost trust in supply chains / the government.

So, the question is, how much of the distortion is caused by more people shopping for spirits in UK supermarkets rather than duty-free, how much was caused by stocking up, and how much was caused by greater consumption (if any)?

As they say, stockpiling won't have benefitted the last 9 months, but the lack of cheap foreign holidays, both in the summer and Christmas peak, with considerable uncertainty in October, may well have done. We can't find RedLeg at World Duty Free or Dufry, which confirms our suspicion they are underrepresented there compared to UK supermarkets.

Similarly, unaudited year-on-year third quarter (October to December 2021) revenues decreased by 32%, but in that period we also reduced support for deep-cut promotional activity in the UK in favour of a longer-term beneficial move to more premium positioning for our key brands. The Board sees the moves made to reinforce the premium positioning of the Group's brands as important for inherent brand and shareholder value.

So they have an excuse for October to December, but of course, they can't know the counterfactual of what would have happened if they'd sold higher volumes at lower prices. All we know for sure is that the LFLs deteriorated further. If they wanted to demonstrate that this lack of discounting was working, then they'd tell us gross profit or EBITDA or something.

As at 31 December 2021, cash balances amounted to £4.1million (unaudited).

This compares to £4.2m at 30th September. Christmas is clearly the peak sales period, but I don't know for sure when they'd receive the cash for those sales.

Although the potential for deep research is strong with a microcap consumer products company, Leo hasn’t bothered with Distil because they always seem to want to spend the profits on developing new products and production facilities. Indeed, in July they went to the market to raise £3.2m for what effectively appears to be a JV with the Ardgowan whisky distillery. Today they said:

We are pleased to confirm that the initial advance of £2.85 million (£3 million less one year's retained interest of £0.15 million) has now been made to Ardgowan under the terms of our loan agreement. Planning for the Blackwoods gin distillery is underway and making good progress in line with our planned timetable. We have also progressed our new Malt Scotch and anticipate formally launching the product in the coming months, opening new market opportunities for the Group and its brand portfolio.

This just seems like an overreach for such a small company. And JV’s have their own set of risks. Later in the report, they say:

I am pleased to report that consumer sales in the UK hospitality sector and export markets began to show signs of recovery in the quarter year-on-year. In addition, we saw good growth in our Ready-To Serve (RTS) product offering:

Now it is the RTS market that always appealed to Leo.

Sales of our Ready-To-Serve pre-mixed cocktails cans increased 150% in the quarter year-on-year, with nine month cumulative sales up by 46%.

This is a great performance and may understate the underlying picture given that pubs were closed in the quarter last year, raising at-home consumption. Conversely:

In the hospitality sector, despite continued uncertainty and staff shortages in outlet, sales increased 542% versus the same period last year and increased 19% versus the same period pre Covid.

Clearly, the 542% figure is nonsense as pubs were closed for much of the period.

Export sales increased by 16% benefiting in part from strong sales in Russia.

And that is due to international travel restarting: These figures almost certainly are dominated by the Bladvod product popular in Russian duty-free outlets. Remember, the Oct/Nov/Dec is their Q3.

Outlook for the full year remains difficult to forecast accurately due to the varying levels of restrictions across the UK and in our key export markets together with mixed economic forecasts although we are anticipating Q4 growth as we lap strong but not extraordinary comparisons.

For us, this company is simply uninvestable because the management lack focus and capital discipline. They have a good mid-market brand with RedLeg and some fantastic potential with cans, but they keep messing around elsewhere and shareholders are never likely to see the returns of any success.

Capital Ltd. (CAPD.L) - Q4 Trading Update

A strong Q4 trading update from Capital, leading them to slightly beat the upper end of their latest revenue guidance range:

FY 2021 revenue of $226.8 million, up 68% on FY 2020 ($135.0 million), slightly ahead of recently revised guidance of $220-225 million (up from $200-210 million guided at our Q2 2021 trading update and up from $185-195 million originally guided at the FY20 results).

The results were driven by strong pricing, strong utilisation, new contracts plus the expansion of existing ones. In fact, every part of the business is delivering above expectations from the start of the year:

MSALABS has had a very successful Q4 2021, cementing a strong outlook for 2022…

The listed portfolio recorded investment gains (realised and predominantly unrealised) of $29.1 million representing a 135% increase over H2 2021…

Q4 saw the strongest quarterly revenues in the Group's history, and the momentum has continued into 2022 across all business units…

Macro conditions continue to suggest sustained strength in the demand environment and outlook with gold & other key commodities still trading at near decade long highs

Perhaps the only disappointment was that the size of the overall rig fleet remained static during Q4. However, they were keen to point out that the three expected rigs were currently being commissioned and this was simply a timing issue. These are in addition to the rigs that are on order for 2022. In previous calls, the number of additional rigs for 2022 was given as 7, but they refused to be drawn on that in this week’s call so this may be now higher. Other snippets of information gleaned from the conference call are:

MSALABS is experiencing exponential growth in line with management expectations.

They doubled their headcount during the year, adding 1000 people with safety performance actually improved.

ARPOR & utilisation are likely to remain high into 2022

Inflation is written into all long-term contracts

Net debt should be down in H2

They will look to extend the buyback if exhausted and a material discount remains.

Broker Tamesis have updated their EBITDA estimate for 2021 from $63.2m to $65.1m based on the beat on revenue. However, this would imply quite significant drops in gross margin for H2 during a period where drilling rigs are in high demand and non-drilling revenue has an increased proportion of high margin labs work. This seems daft to Mark, who expects the real 2021 EBITDA to be closer to $70m than $65m. (Although Tamesis have corrected the error with the net debt estimate that was in their previous note.)

For 2022, an average of 90 operating rigs at the current $184k ARPOR plus say $84m mining services revenue would be $282m total revenue, probably generating around $90m EBITDA and over 17p EPS, assuming cost inflation is relatively contained. If past years are any guide, then we would expect Capital to estimate more conservatively than this at the start and then upgrade during the year. The Tamesis 2022E EBITDA currently remains at $71m from prior to the Q4 trading statement, and while they were always unlikely to upgrade without the revenue guidance from the company, pretty much all of their estimates now look too low for 2022.

All this means that all of the broker targets are likely to be some 15% or so below where their fair value multiples suggest they should be. And that is before you consider that all brokers currently value MSALABS at a sub 5x EBITDA multiple despite growing revenue at 100% pa! Upgrades are therefore likely to follow the publication of the full results in mid-March, although they will probably still undervalue MSALABS in their models even after that.

As is now usual with Capital, the market has underreacted to this trading statement, with perhaps a seller taking advantage of the higher volume that this trading update brought to exit an illiquid position. However, the company is in a better position than in the recent past since it is now generating quite prodigious free-cash flows which are being directed, at least partly, towards share buybacks. Given the potential here, the more stock they can buy back at current levels, the higher the long term rewards that will accrue to the business owners.

Sanderson Design Group (SDG.L) - Trading Update

Whilst Group revenues for the year are expected to be only slightly ahead of Board expectations at approximately £112.0 million (FY 2021: £93.8m), the Group's profitability is expected to be significantly ahead owing to the operational gearing effect of recent manufacturing sales and additional, higher margin, licensing income.

As we have seen with Games Workshop, licensing income can be unpredictable. Sanderson put licensing income through as revenue but, of course, it goes straight to the bottom line. In this case, it looks like revenue would have grown without the licensing income, although only to the same levels as 2018/19/20 (i.e. pre covid).

Overall brand product sales during the year have performed broadly in line with expectations, with a particularly strong performance from the Morris & Co. brand. North America recorded strong growth of approximately 40% in constant currency and represents approximately 19% of the Group's brand product sales.

In the H1 results, they have a brand-by-brand breakdown of sales North American increases. If this is not one-off covid effects and rather part of a pattern of sustainable growth, then North America would now be the growth driver going forward.

The Group's manufacturing operations have continued to benefit from very strong order books. Third party sales are expected to be up approximately 33% in the year compared with the prior year, in part reflecting the attraction of onshore UK production for UK customers following Brexit and COVID-19 related global supply chain issues, along with strongly growing international sales. Both of the Group's manufacturing sites, wallpaper printing in Loughborough and fabric printing in Lancaster, performed well.

Clearly, the 3rd party manufacturing business will be a margin-taker, and while this is a positive right now with tight supply, that will not always be the case.

Licensing agreements signed in the second half of the financial year, including a further agreement with NEXT announced in October 2021 and an agreement with Williams Sonoma announced in August 2021, contributed to a strong performance from licensing.

So, the question arises when will the revenue be recognised from these deals? Again, with Games Workshop, we have seen large minimum guaranteed licensing income built into contracts. This is recognised immediately and will mean there is a long gap before any further payments are made. It also means that revenue recognition is brought forward whether or not cash has been received.

This performance reflects the recognition of accelerated income under IFRS15 along with robust sales from existing licensees, notably NEXT's Morris & Co. womenswear and the core categories of window coverings and bedding.

Ideally, we would know how much of this minimum guaranteed licensing income has been covered by sales made by the licensee. Without that, it is very difficult to know whether there will be any recurring revenue at all in future. However, there was this snippet at H1:

Accelerated licensing income under IFRS 15 was £0.5m (2020: £0.3m; 2019: £2.0m).

So maybe there are some adjustments you can do yourself to find the potentially recurring part if you wish.

As a result of the above, the Board expects adjusted profit before tax of at least £12.0 million for the year ending 31 January 2022 (FY 2021: £7.1m).

Approx. 14p EPS after tax.

The Company's balance sheet has further strengthened during the second half of the year. The net cash position at 31 January 2022 is expected to show an improvement on the £15.4 million, excluding leases, as at 31 July 2021.

This is the sort of company that might have a defined benefit pension liability, and in any case, it is always worth checking in the Annual Report:

The Group made additional payments to the pension schemes of £2.1 million (2020: £1.9 million) to reduce the deficit, as part of the ongoing planned reduction.

The triennial valuation of the defined benefit schemes is due to be carried out based upon the schemes’ position on 5 April 2021.

Not the best moment. Although some consideration will be given to interest rate rises since. The gross pension size is £85m. Similar to the company's Enterprise Value prior to this week’s rise, so relatively large. And there appears to be a bias towards UK equities in the pension.

The Company has agreed a Recovery Plan to pay contributions of between £1,500,000 and £1,900,000 per year to eliminate the funding shortfall by October 2026.

So interesting that they paid £2.1m in FY (Jan) 2021. So it seems they are having continuous discussions with the pension trustees. This reduces the risk from the upcoming triennial. Clearly, you can assume this will be kept to, apply your discount rates and work out what the equivalent perpetual annual payment would be, but I'm going to go for about £1.0m. So, the real PBT is £11m and EPS around 12.5p.

This works out to be a current P/E of 15. Further analysis may show that this is on the cheap side of fair value, but it isn't immediately obvious, and buyers today have to be fairly sure that this is the start of a multi-year growth trend, not simply a return to the rather pedestrian trading prior to covid.

Gattaca (GATC.L) - Trading Update

The mid-cap recruiters have been going great guns recently, with the likes of Robert Walters (RWA.L) hitting all-time highs. Sadly, not all recruiters are created equally. As Gattaca have shown this week with the following trading update:

Following a review by the Board of the outlook for the business for its financial year ending 31 July 2022 ("FY22"), it now anticipates the Company's continuing underlying profit before tax will be significantly below market expectations. This is driven by delayed recovery in our contract business where the improvement in our customer's demand has been slower than expected we now foresee a lower growth rate in the second half of the financial year.

For what these expectations were we turn to Equity Development who were forecasting £6.1m adjusted PBT and 14.4p EPS. Now Gattaca say:

The Board expects H1 2022 NFI will be around £22m (H1 2021 £20.5m) and FY22 NFI to be around £45m (FY2021 £42.1m), with continuing underlying profit before tax for its financial year ending 31 July 2022 to be around breakeven. We remain committed to driving sustainable recovery from the pandemic and confident in the long-term growth prospects for the business.

So that is quite a reduction, from £6.1m to zero. And you can see why the share price was down 36% on Tuesday to around 90p.

We always found the Equity Development price target of 275p to be quite fanciful, as it was based on applying EBIT multiples to 2024 Estimates as if they were already in the bag. Comments in the previous note, such as the following, don't read particularly well in light of today's update:

In fact, we are tempted to upgrade our FY22 forecasts (see quarterly NFI chart below) & 285p/share valuation, but instead have erred on the side of caution. Preferring to keep our powder dry, until there’s little risk of a new dominate strain pushing the recovery to the right over the winter months, &/or disrupting client recruitment plans.

More bagholder than in the bag, it seems. Gattaca could have chosen to blame COVID but didn't, simply saying:

While it is taking longer than anticipated to rebuild our contractor volumes to pre-pandemic levels, our investments in technology and sales headcount have ensured Gattaca is well equipped to meet future requirements as the contract market recovers.

Equity Development released updated forecasts later in the day, in a note that blamed the UK economy for Gattaca's weakness:

Like many things, the economy rarely moves in straight lines. Prior to the latest lockdowns, experts were forecasting a powerful rebound in UK GDP, as workers fully returned to the office. However, although ‘Britain might rule the waves’, it has little control over the direction of the wind. In fact due to the latest Omicron outbreak, the pace of recovery has temporarily hit a soft patch.

Strange how other UK recruiters haven't noticed this soft patch!

Not all is lost with Gattaca though. While no one in their right mind would base their investment case on updated ED forecasts, today's fall brings them closer to trading at Tangible Book Value again. The vast majority of that book value is cash and receivables. And Net Fee income is actually up vs FY21 (although nowhere near pre-pandemic levels), and part of the reason for the poor profitability is the increase in headcount:

In the contract side of our business, which historically represents 75% of Group NFI, we have continued to invest in people ahead of demand, with UK sales headcount up 24% since January 2021.

So if the share price falls back much further, taking it below Tangible Book Value, this could start to look like a good value play again. At least for the patient investor willing to wait for a recovery in trading. The history here suggests you want a decent margin of safety, though. It dropped to 30p in the initial COVID panic, although this proved to be a very good entry point.

Pressure Technologies (PRES.L) - Full Year Results

We last looked at Pressure Technologies following their interim results when they flagged that a decent H1 was not going to be repeated, with orders slipping from 21 into 22. As a result, broker N+1 expected a H1 EPS of 2.9p to turn into a full-year loss of -3.9p EPS.

However, they didn't increase 2022 estimates to reflect the supposed spillover of work into 2022. In light of this, we thought a wait and see approach was best.

With the share price down 30% since then, that turned out to be the best strategy, particularly since this week's results show a bigger loss than forecast, at least on an unadjusted basis:

They highlight a lower adjusted loss of £0.7m which exclude amortisation, a loss of property value vs book value, what appears to be a failed ERP system, plus:

Reorganisation and redundancy costs in the year were £0.4 million (2020: £0.4 million), which predominantly related to the PMC site reorganisation costs that took place in February 2021.

Other exceptional items included an inventory write off in CSC relating to obsolete stock items totalling £0.2 million (2020: £0.5 million), costs related to the closure in the prior year of PMC's Quadscot facility of £0.2 million (2020: £0.7 million), and other head office costs including bank refinancing costs totalling £0.2 million (2020: £0.4 million).

While we are sure many of these are really one-off, they mostly appear to be the result of poor decision-making in the normal operations of the business, so excluding them would seem a little optimistic.

Net debt has dropped, but this is due to £7m (after costs) of new equity raised during the period. However, the good news is that it has repaired the balance sheet which looks stable enough to bear the losses for at least a while yet.

The outlook is perhaps less inspiring than it could be:

CSC has a strong defence order book going into FY22, with high-value projects weighted to the second half of the year.

It is defence orders that slipped from 2021 into 2022, so flagging a H2 weighting doesn’t give a lot of confidence that targets will be met. On the Hydrogen side:

Hydrogen related revenue was strong in FY21 and the pipeline of opportunities for static and mobile hydrogen storage systems with established and new customers continues to grow. The visibility of future demand is improving, with refuelling station projects expected to ramp up sharply driven by city bus networks from 2023 and accelerating heavy duty truck demand from 2024.

But this is exactly the sort of new technology roll-out that tends to end up taking much longer than planned - and Pressure are not driving the change, merely receiving orders. On oil & gas they say:

For PMC, our focus remains on the recovery of profitability and cash generation. We are encouraged by recent increases in order intake for the Roota and Martract businesses and by efficiency and margin gains achieved from operational improvements at all sites. Our major OEM customers, including Schlumberger, Halliburton, Expro and Baker Hughes are reporting a stronger outlook for the oil and gas market during 2022, which we expect to drive improved performance...

This makes sense, we have commented in the past how this oil cycle is different since investment is being driven by reinvestment of excess profits, not by debt or equity issuance.

Ongoing investment following the December 2020 fundraising is helping to deliver operational improvements that will underpin the capacity growth, efficiencies and reduced lead times at our Sheffield facility over the next two years in readiness for the increasing hydrogen demand.

While this sort of statement may be viewed highly positively in a company with a strong history of good capital allocation, but Pressure is not that type of company. Perhaps more by fortune rather than any good judgement, Pressure may find itself in a favourable position in the next few years with hydrogen, defence and oil & gas all in strong cyclical up-trends. However, with the dreaded H2-weighting already being flagged for 2022 and no meaningful hydrogen revenues until 2023, the wait and see approach remains the best option here.

Ramsdens (RFX.L) - Annual Results

In their pre-close statement in October Ramsdens said:

The Group has continued to control its overheads and with the benefit of government support during the Period, the Board is pleased to announce that it anticipates, subject to review and audit, reporting profit before tax of at least £0.5m.

We weren’t particularly impressed with that given the level of government support they must have received in the period. The above £0.5m turned out to be £0.6m in the results. Here are the other headlines:

The actual level of government support wasn’t that material:

The Group received £1.6m of Government Support during the year, including £1.5m through the furlough scheme to assist in retaining jobs.

But still interesting that they choose to pay a dividend. perhaps the political climate that made this a no-no has moved on to more pressing matters. The reason for the relatively limited government support was that, unlike the 2020 lockdowns,…

The Group kept almost all stores open through the retail lockdowns and continued to provide essential services that offer financial support to our loyal customers.

So effectively a break-even performance which means there is still a long way to get back to where they were pre-pandemic. Especially in travel:

Travel restrictions were tougher in summer 2021 than in summer 2020, significantly impacting foreign currency exchange volumes. This resulted in foreign currency income approximately £10m lower than pre pandemic levels.

There are some areas doing well, though:

The investment in the Group's online retail jewellery operation has led to online sales more than doubling year on year.

And in the Q1 trading update that accompanies these results they lead with the Jewellery retail side:

The Board is pleased to provide an update on Q1 FY22 trading (October to December 2021).

· Investments in our jewellery retail operations have continued to produce strong results.

o In store retail jewellery revenue up more than 30% on October to December 2020.

o Online retail jewellery revenue up more than 70% on October to December 2020.

The problem is that FX was at least half the profit before covid and this is still nowhere near where it was:

Foreign currency volumes were approximately 40% of pre pandemic levels but had increased by almost 200% on October to December 2020.

Covid has accelerated trends to a cashless society that were already in place prior to covid. Ramsdens also offers prepaid travel cards and international bank-to-bank payments however they are still overwhelmingly a supplier of cash foreign currency, in-person, to the lower demographics. Given cashless trends, Brexit, testing requirements, and the cost-of-living squeeze their typical customer is likely to be demanding less FX cash than previously.

All of this means that a full recovery for Ramsdens is likely to be to a lower level of profitability than they previously enjoyed. Stockopedia has 12.8p EPS forecast for 2022. Without doing a lot more work it is hard to confirm how realistic that is but it wouldn't seem out of place. The balance sheet is rock solid with 41p/share in cash which makes this on a forward P/E of around 10 adjusting for that cash. Investors could do a lot worse in the current market.

Mark struggles to get excited by this rating, however. Just prior to the pandemic, when the share price was at its peak of around 250p the company had a forward EPS of 21.4p and had 36p/share in cash. Which is almost exactly the same rating as today.

At its peak, it was a 10xP/E stock, and it is today. And we don’t subscribe to the theory that investors should pay significantly higher multiples for small cap stocks today, simply because the average small cap is overvalued.

Best of The Best (BOTB.L) - H1 Results

These are to 31st October and had already been guided in November, when they said:

The Company reports that financial performance for the period is in line with the market guidance issued on 13 August 2021. Customer acquisition costs have stabilised, albeit at the higher levels previously reported. Engagement from the enlarged player base has also normalised, with average order values and frequency similar to pre-pandemic levels. Trading for the period has, therefore, been consistent with management's revised expectations.

Those expectations (from finnCap) were FY revenue £40m and 53p EPS. In these results they say:

Total revenue for the six months £19.12 million (2020: £22.09 million), in line with management's expectations

This seems a little light given that they entered the period with the tailwind of a massively increased, but rapidly attriting customer base. Profits were strong, however:

· Profit before tax £3.04 million (2020: £6.80 million), in line with management's expectations

· Earnings per share 27.26p (2020: 59.84p)

The balance sheet is very straightforward. Most of the PP&E is "display equipment", which you'd probably want to write down to zero, but apart from that, you've basically got £8.3m cash and £3.6m payables. No long term liabilities whatsoever. Potentially there is a few million spare cash that could be distributed, and certainly, there is a large enough buffer to see them through short term issues or take advantage of opportunities.

But with the share price down nearly 40% on the day, clearly something is wrong...

Following a period of stabilisation (albeit at a significantly higher level than pre Covid), the cost of acquiring players increased by a further c. 37% in November and December 2021 compared to the prior six month average, resulting in fewer customer registrations for similar levels of marketing investment.

After being told in November that the marketing had stabilised, this is very bad news. That 37% is incremental to previous increases. What they haven't told us is what engagement from the player base and attrition is like. Early January 2022 indications suggest that marketing costs may be trending back towards levels experienced in the period under review. Well, they stabilised for 2-3 months and then deteriorated again, so we're hardly going to read anything into 2 weeks. Confidence will now be low until things have been stable for over 6 months.

reduced customer acquisition in November and December 2021, together with a cautious outlook means that we believe our revenues for the full 12 months will now be £34 - £35 million, with pre-tax profits expected to be £4.25 - £4.75 million.

The implication is that customer attrition is very high for difficulties in acquisition over just 2 months to cut revenue by 26% over 6 months.

We are a profitable, cash generative business with no debt and a large and loyal customer base. We will be taking steps to reduce the bottom line impact of reduced revenues by maintaining a sharp focus on costs, and prioritising only the most efficient marketing channels.

This should now be one forecasting scenario - what happens if they slash marketing costs and just run their "loyal customer base" for profits? But that's certainly not what they did in H1: administrative expenses including marketing was actually 10% higher than 21H2. Unfortunately, unlike many other companies, there is absolutely no breakdown of admin expenses (apart from the director and auditor costs), so we've no idea how much they spent on marketing. They also fail to publish any KPIs, either today or in the annual report, so we have no idea of:

Number of active customers

New customers

Attrition rate

Customer acquisition cost

Customer lifetime value

This makes it exceptionally difficult to forecast the future. The brokers' note gives some more information:

we are cutting our EPS (Dil. Adj.) forecasts by 25% to 39.9p for FY22E, by 32% to 43.9p for FY23E and by 35% to 49.3p for FY24p as we conservatively assume little change to current trading.

So important to note that forecasts are based on little improvement and that they think/claim this is conservative.

BOTB is facing three pressures: (1) the decay from last year’s new cohort of new customers (which is tracking in line with expectations, but last year was a COVID-driven bumper year), (2) increased cost of sales because of higher prizes and new competitions and (3) rising marketing costs with Meta (Facebook and Instagram) hiking prices and reduced efficiencies caused by IOS14. The 4Q21 average customer acquisition cost has risen 2.4x to £50.36 from 4Q20 and is quadruple that of 2Q20.

(2) was not mentioned in the update at all. (3) provides considerable more detail than in the update. Obviously, they have got this information by talking directly to the company rather than pulling it out of a hat.

From the FY report, they claim to have a database of 1.7m people. If you assign a value of £50 a person then that's £85m versus the closing market cap of £38m (and adjusted EV of maybe £34m). But clearly, that would be insane because that database will include people who have not played for years, and we daresay more than a few duplicates. And saying the acquisition cost was £50 does not mean that those players are worth £50 to the company today.

The Profit Before Tax guidance implies a reduction in planned marketing expenditure and is also dependent on a tight focus on costs. But finnCap's forecasts imply some rather strange numbers here:

So, we are expected to believe that gross margin will collapse from 56.8% in H1 to 37.3% in H2? It was 56% in 2019 when they were still operating in airports. The only explanation we can see is:

(2) increased cost of sales because of higher prizes and new competitions

They are forecasting approximately the same absolute cost of sales in H2 as H1, but on much lower revenue. Cost of sales is primarily prizes, which are decided before they know how many tickets will be sold. More prices help sell tickets both at the time and in future and are so a kind of marketing cost. But why would a company do that if they are saying:

We will be taking steps to reduce the bottom line impact of reduced revenues by maintaining a sharp focus on costs

Anyway, what finnCap do expect BOTB to cut is advertising costs, with a 48% cut in total admin costs implying these must be slashed by 70% or more. Again, this seems unlikely.

It is very easy to sort out the gross margin whenever they want: just reduce the number of prizes! Leo is forecasting a 45% margin for H2 (52% FY) recovering back to 55% by 2024. (so he thinks gross margin will be higher than finnCap imply.)

But admin costs could be harder to cut - some will be marketing staff, and I think they need to keep advertising in some form, it is just a matter of making it more effective. The base case is surely that this settles at a significantly higher level than it was in 2019, supporting maintained higher sales. Nonetheless, Leo sees sales drifting lower - £24m in 2023, £20m in 2024 as the customer base decays.

Barring any genuine stabilisation/cut in acquisition costs, Leo only gets a DCF valuation of 185p, though this is on conservative assumptions. They could do themselves a lot of favours by providing the data to model properly since clearly neither they, nor finnCap, are up to the job themselves (although, to be fair, it isn't their job). finnCap say:

Should the share price continue to weaken, it would make good sense for BOTB to consider share buybacks, rather than special dividends.

That might be them mirroring what the company have said, or it might be them hoping to simply sell them some more services.

Revolution Bars (RBG.L) /City Pub (CPC.L) - Trading Updates

Many other hospitality companies have been reporting better than expected Christmas trading, so we were interested to see how Revolution Bars have done. Previously they had been reporting modest catch-up trade with the earlier part of the period up 14% on 2019. Perhaps their younger audience will have been particularly resilient?

Sales over the Christmas period were impacted by the move to 'Plan B' including the return to the 'Work From Home' instruction, implementation of Vaccine Passports for late night bars and government messaging which unhelpfully encouraged the limiting of social interactions. LFL sales for the 6 week period ending 1 January were -23% when compared with the same period 2 years ago, the last unaffected Christmas period.

Oh dear! Not great. But how does it compare to City Pubs, who also reported this week:

a restriction free October and November saw trade returning to 2019 levels. December began well with greater pre-booked business than 2019, however the emergence and onset of Omicron reduced sales to 85% of 2019 during this important period as most office party bookings were cancelled. The strong trading in October and November helped to offset any reduction in December.

So Revolution were down 23% for 6 weeks including the end of November when there was no Omicron effect and City Pub said things were going well. Whereas City were down only (approx) 15% and that's just in the worst four out of those 6 weeks. Clearly, Revolution have massively underperformed here, yet again, despite having a younger demographic.

Perhaps location played a part though? City's pubs have a South and especially London bias compared to Revolution which are in city centres across the country. We suspect this is probably the big difference though:

implementation of Vaccine Passports for late night bars

The administrative awkwardness of obtaining a vaccine passport with paper certificates on inexplicable short expiries, an app that keeps logging out and ridiculous hoops to jump through just to register a LFT, probably means that this was more a matter of "can't be arsed" than "refusing to vaccinate or test". Basically in a large group, there is always going to be somebody who has forgotten their password, or has a flat phone battery or doesn’t know what they are doing, with no way to recover in a reasonable time.

Revolution:

The impact of the Government actions was most felt in the cancellation of office parties. Pre Booked Revenue, an indicator of Corporate Christmas parties, was -39% for the 6 week period to the 1st January 2022 when compared to 2019/20.

But...pre-booked parties will generally be in the evening whereas covid passes only apply when turning into a nightclub around 1am. While they hope people will stay, I doubt they manage to continue tracking whether they started off pre-booked or not.

City:

most office party bookings were cancelled

So looks like City were hit harder by office party cancellations. So, the evidence appears to be that, once again, revolution underperformed because their offering is missing the mark, not due to external temporary reasons. Their answer to this? The same as always: throw more money at it.

Our refurbishment programme has continued as planned and we have completed 6 refurbishments and are pleased with their early performance, with a further 13 to complete in current financial year.

This was supposedly a well-invested estate going into covid, which was then left mostly empty, only needing them to blow off the cobwebs.

Cash, net of bank loans, was £4.7m as at 19 January 2022 following the utilisation of a portion of the funds raised last year on our refurbishment programme.

Cash is up quite a bit since 3rd July when they had £3.6m net debt, which is good news. Some of that £8.2m cash between those dates will be because 3rd July was immediately after payday, whereas 15th November is mid-month. Assuming they are paying monthly VAT then there is a similar effect there also. On the other hand, repayments of deferment of VAT of maybe £1m (missing from the debt figure) were made.

Given their strange year-end, it really is difficult to draw firm conclusions, so we think the main takeaway is to be aware that "net cash" by itself is of limited use to the investor. Nonetheless, it must be acknowledged that cash flow has been strongly positive since the year-end, but perhaps poor in what should have been their peak trading period. And this performance was of course achieved in the context of a reduced 12.5% VAT rate, which is due to finish on the 1st of April.

If Revolution survives then potentially at some point there may yet be an opportunity to buy here. But so far there is little evidence that they are able to make real profits with their current estate and model. While the question with RBG remains whether they are worth anything, City Pub Group are more focused on arguing that they should be worth more. They say today:

The Group is pleased to report that following a valuation by the directors, the pub portfolio returned equivalent of 150p net asset value per share. A more formal exercise through independent valuers recognising our 90% of invested freehold based estate will be reported on at our full year results in April.

This compares to a share price of 115p at the moment, so could be interesting to those like asset plays (and who believe the valuation for freehold pubs in the current environment is strong.)

Parity (PTY.L) - Trading Update

Parity is a subscale recruiter that tried to move to higher-margin consultancy work before making a hash of it and is now trying to return to its "core recruitment capability". This week’s trading statement has been well-received, though, with the share price rising 15% on the day, presumably as they say:

...the Group is pleased to confirm it has met or marginally exceeded market expectations for FY2021.

Here is the detail:

· Group revenue is anticipated to be slightly ahead of the £47.6m target.

· Net Fee Income ("NFI") in line with expectations of £4.1m

· The Group anticipates a modest Adjusted EBITDA profit, instead of an expected small loss.

As a recruiter, you really need to be focussing on the NFI, not the larger revenue, which is mainly pass-through. In comparison, Gattaca that we looked at above is forecasting NFI of around £45m, which shows how much of a minnow Parity is.

Still, they now indicate that they will be profitable rather than loss-making, but hang on, they actually say a modest Adjusted EBITDA profit. So that is still a small loss then on an actual accounting basis! Indeed, at the half-year, an Adjusted EBITDA of £251k ended us as a Loss Before Tax of £491k - partly due to the management change costs of their previous failures.

Through improvements in working capital management the Group closed the year with an improved Net debt (pre-IFRS16 adjusted) position of £1.2m, ahead of market expectations.

Sounds good until you realise net debt was £1.1m at the half-year. And overall the balance sheet is weak here. So paying 2x Sales for a subscale recruiter looks bonkers. However, at this end of the market, anything can happen. For example, their competitor Triad appeared to hire a guy who wrote the word "Blockchain" on his CV and their share price went up 4x, largely as a result of them announcing this.

However, in this case, the most likely "anything" is a placing to keep the lights on, sorry I mean invest in…

…extending its sales and marketing capacity to drive innovative recruitment solutions to meet the growing demand for highly skilled resources across data, technology and change management.

Normally, at this point, Mark would comment that it's nice work for their broker finnCap. However, in this case, they are so subscale their placing fees will be a rounding figure in the finnCap accounts. In summary, if you want a struggling recruiter with patchy profitability, buy Gattaca. It is on a much lower Price to Net Fee Income rating, has net cash instead of debt and has greater scale.

Smiths News (SNWS.L) - Business Update

This is effectively an AGM statement:

The Board is pleased to report that overall trading in FY2022 to date is in line with market expectations, with the key elements of sales, sustainable efficiency savings, operational cost controls and health and safety performance all collectively on track.

If you were the management of Smiths, you could possibly feel a little aggrieved that the market has reacted positively to this in-line statement. It is as if the market has got used to them struggling and is pleasantly surprised when it isn't a profit warning!

There have been uncertainties though, and as a low margin distributor reliant on lorry drivers to make deliveries, the risk probably was to the downside recently. So that they are coping ok with these pressures is good news. They also remind us of the progress they are making:

The first strategic priority, to reduce bank net debt to below 1x Adjusted pre-IFRS16 EBITDA, is expected to be achieved by the half-year, marking a key milestone. In recognition of this significant progress, in December 2021 the Company's banking facilities were favourably amended, extending the term by 1.75 years to August 2025 and allowing for a greater share of free cash to be distributed to shareholders.

Although this is a known known.

Mark does think there is value here. But perhaps not to the level that those who rely on simple metrics such as P/E think there is. Since it is a melting ice cube, investors have to do their own DCF and not rely on more basic metrics. When Mark does that he gets a value somewhere above 50p. So, yes, a decent upside from the current 40p share price, but perhaps not an exceptional one.

Restaurant Group (RTN.L) - Trading Statement

Until recently they were most famous for the failing Frankie and Benny's brand. In June 2020 they announced the closure of more Frankie and Benny's sites than Carluccio's ever had. However, they had already been trying to move away from their tired brands by buying Wagamama, completed on New Years Eve 2018. There was much criticism at the time, focussing on the logic of a lowly-rated company with a reputation for running brands into the ground issuing equity to buy a highly rated rising star. Today they have a trading update.

In TRG's last market update on 16 November 2021, the Group provided guidance that on an IAS 17 basis it expected FY21 Adjusted EBITDA to be a range of £73m-£79m and FY21 year-end Net Debt was expected to be less than £190m. The Group is pleased to announce that due to good cost control and continued strong trading relative to the market, management now expects the Group's FY21 Adjusted EBITDA will be at the top end of the range and FY21 year-end Net Debt will be less than £180m.

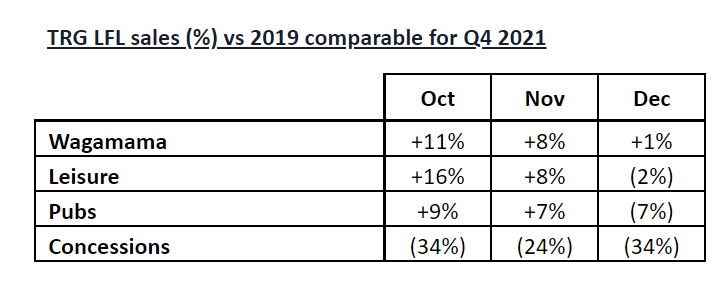

So maybe a little better than Hostmore which was merely inline?

Well isn't that interesting? Wagamama sales are up 1% whereas TGI Fridays were down 8% in December. It is almost as if quality and service count for something! Though clearly being positioned as the next Nandos, Wagamama seems to have maintained good ratings in the locations we spot-checked - far higher than TGI Fridays anyway.

Even the remaining Frankie and Benny's have decent reviews and together with the rest of Leisure only fell 2%. "Concessions" are mainly situated at airports and in Leo’s experience, many were closed. There was certainly a Gar funk-all open when he went through Birmingham airport recently.

Despite the near-term uncertainties, the Board remains confident in the Group's prospects given the strength of our brands, substantially reduced net debt and outperformance versus the market.

The Group's next scheduled update is the preliminary results announcement on 16 March 2022.

The main good news here is the quantitative evidence that they haven't broken Wagamama, at least not yet, and that their other leisure brands might even be improving. Unfortunately, at first glance, their valuation reflects this with a 2022 P/E of around 30x. And they carry a significant amount of debt and lease liabilities, despite a number of CVAs at the brand level.

Appreciate (APP.L) - Q3 Trading Update

As background, things looked extremely hairy at the point of issuing their annual report in August. In the Going Concern Disclosures they said:

The Base Case requires the group to draw down on the RCF in the period, with the lowest headroom being £4.9m in September 2022.

In the most extreme downside scenario 6, the Group would breach its headroom by £2.3m

You can read the details in the annual report, but the base case seemed pretty optimistic to me and scenario 6 (or equivalent combinations of badness) not-at-all unlikely. Off the back of what looked close to a "material uncertainty over going concern", the share price inexplicably surged from 34 to 40p.

Fortunately, things picked up a little by H1, but the big win was:

During the six months to 30 September 2021 a review of the ring fencing of balances in relation to digital code was undertaken. These products are not regulated products but the balances had historically been segregated from AG cash balances and the amounts segregated had grown significantly over the last 18 months. The review concluded that there was no regulatory requirement to ring fence balances and no contractual requirement, other than for one particular customer. Therefore, in September 2021 £11m of ring fenced funds were transferred to free cash.

While good for shareholders, this would serve as a critical warning never to buy "digital codes" which are spendable on their app as gift vouchers. In their outlook they concluded:

We typically see about a quarter of billings in the first half of the financial year and around three quarters coming in our second half, and I am confident that we will deliver our expectations for the financial year.

Overall, billings for Q3 FY2022 up to 21 November are £37.0m (FY2021: £39.4m) (FY2020: £43.9m), with an improvement in November to a level which is closer to the previous years

Pretty much immediately after that Omicron emerged. Although most of their billings come in pre-Christmas ready for Christmas, if people don't spend the vouchers then (in most cases) they can't recognise the revenue. And if they have leftover vouchers they are not going to buy more, including as part of Christmas savings starting around now. So the fact Omicron didn't turn out as badly as it could have done is very good news for them. This is reflected in the trading update issued on Wednesday for Q3 ending 31st December:

Underlying Q3 billings* of £96.1m were 13% ahead of Q3 FY20 (£85.1m) and broadly similar to Q3 FY21 (£96.8m)

These figures are at or near all-time highs. The consumer side is slightly down on strong comparatives. Cash looks particularly strong, but of course, is flattered by something in the order of £10m of reclassified cash.

Free cash as at 31 December 2021 stood at £36.0m (31 December 2019: £19.1m; 31 December 2020: £33.5m)

We regularly highlight the risks of ERP projects to companies. They've spent at least £6.2m on this so far and it has been delayed at least once. We have no real way of knowing whether this is actually working here:

The first phase of the Enterprise Resource Planning implementation was successfully delivered earlier in January 2022. This replaced the legacy back office systems that support our HighStreetVouchers.com website and will enable us to operate more efficiently, whilst underpinning our plans for growth.

The success of this Christmas campaign is key. Once people start their regular savings, cancellation levels are very low giving excellent revenue visibility - effectively it is a forward order book. They say they will update on this in the year-end trading statement expected in April. Here is the current outlook:

· We are on track to deliver in line with our expectations for the year as a whole.

· The momentum seen in Q3 has been continued in the early weeks of Q4 with underlying billings ahead of the previous two financial years as at 17 January 2022. These are 8% up on FY20 and 10% higher than FY21.

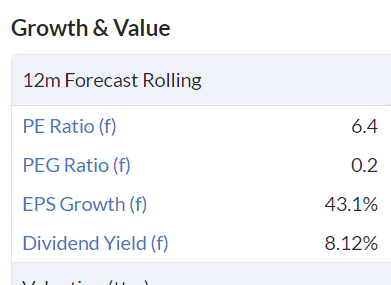

So it looks like they have survived covid and the share price is now about 25p versus that 40p when they looked in serious trouble. Of course, that does not mean they are cheap now, but they look good value on Stockopedia metrics:

And these forecasts now look fairly conservative, with H1 revenue at a recent record and billings at highs. They hold large amounts of customer cash, £207m at the end of September, and £181m on average across a typical year. Historically they have earned significant interest on this cash, but this has been ever decreasing since the financial crisis. Each rise in bank rates of 0.25% is now worth £0.5m a year to them, straight into PBT. With real interest rates currently at negative 5.15%, there does seem to be considerable scope for them to rise. For example, a rise in rates to 2% would add nearly £4m to their PBT, or 1.7p EPS. And since they withdrew hampers from their offering, they have no adverse exposure to inflation or direct exposure to supply chain issues.

There also seems scope to further cut costs after having withdrawn from hampers and other businesses, and due to the switch from paper to electronic gift vouchers. Amortisation on that CRM system will cost them, but most of that money was probably wasted and best written off now in any modelling. They have said they'll stand by their 50% dividend distribution policy. So I could easily see this yielding 10% this year.

Unlike many other businesses, they haven't had to issue more shares, and the abandoned parts of their business were relatively small and unprofitable. So there is no obvious reason why they couldn't regain pre-covid share price levels of 75p. The CEO bought this week, albeit only a token amount. So, in our opinion, this is worth doing some more detailed modelling on.

That’s it for a monster SCL news week. We are expecting next week to be equally frenetic, so enjoy a weekend of rest from the markets.