Small Caps Live Weekly Summary

Online Sales, SYS1 MORE CRL APP MPAC JOUL PMP SDG VNET

WayneJ was back this week with a Large Caps Live looking at some of the ONS consumer data for online sales, plus it was a busy week for small cap news.

Large Caps Live

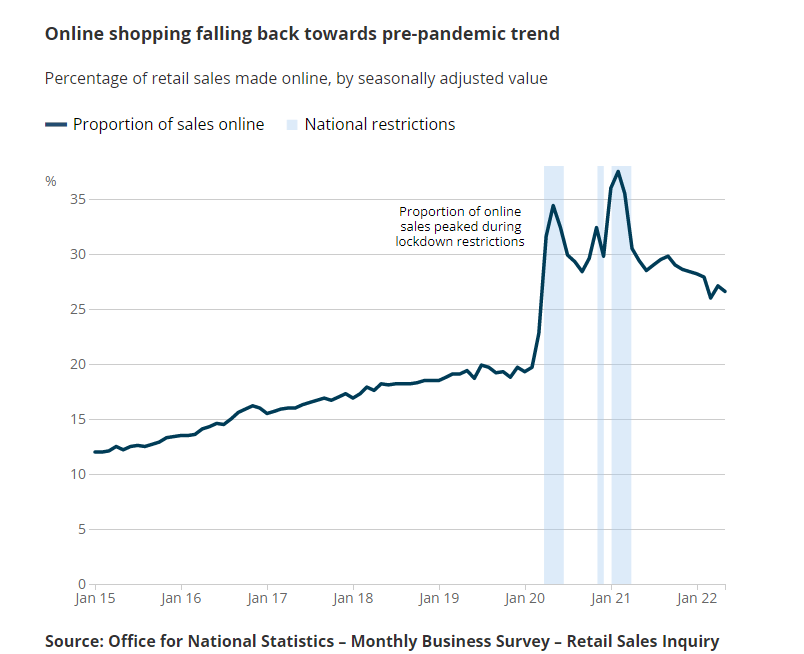

So the first thing I think it is worth highlighing today is a tweet from the ONS:

The actual report is here. I am going to punch up a couple of charts as I think they have implications on retail and general consumer spending.....

So, a couple of points:

(1) In the most favourable conditions ever for online spending - 37% or so of retail spending was online. That seems to me to give a 'maximum' at least for the next few years unless there is much change in retail structure (which we will touch on shortly).

(2) We will come shortly to overall spending in value terms but taking for granted it is not much bigger in the last few months (ie not increasing in value) it does make me wonder if some of the dash for warehouses for online shopping may reverse (implications for Somero perhaps but more importantly for the big retail warehouse landlords like Segro). A lot depends on how the increased demand was met. If it was smaller, less efficient warehouses that are now being upgraded, this could mean the cycle is still not on the downslope.

(3) I have still not got my head around the amount of labour required for an online sale vs a physical shop. But my suspicion is that maybe 100,000 additional jobs or more in the UK and lots more in the US got created by online retail. And that the above chart might suggest that some of them will start unwinding.

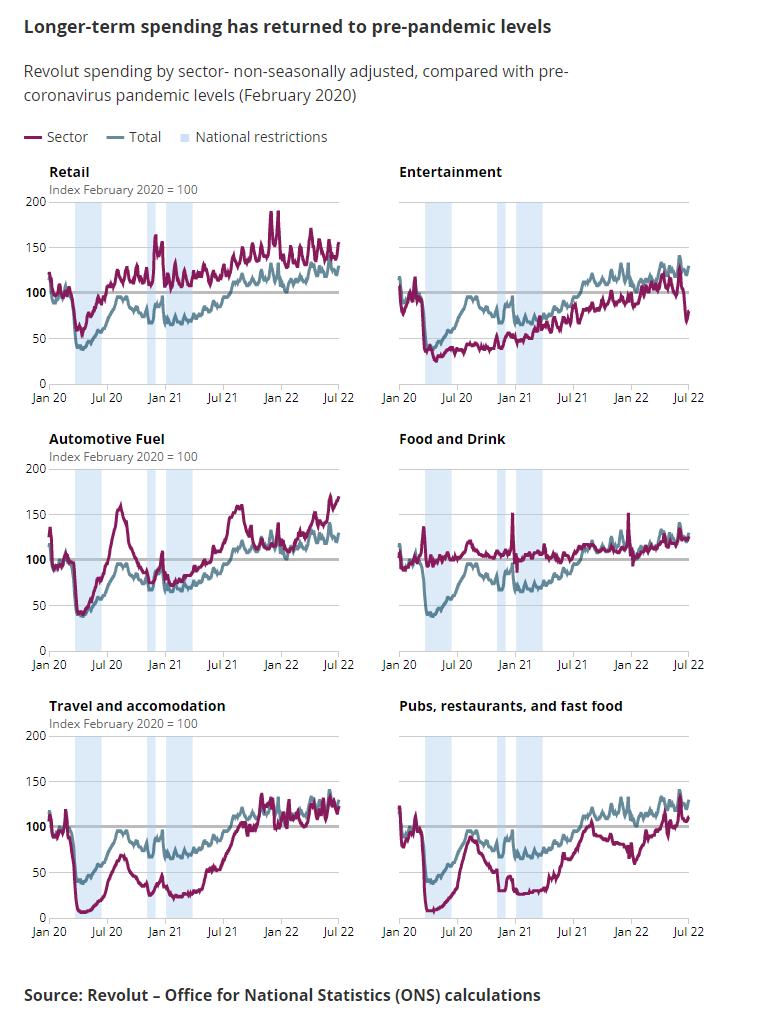

(4) This chart shows data from Revolut - which in itself is interesting - it looks like ONS has access to Revolut credit card data.

(5) The text at some point highlights that Revolut customers are younger etc. But nevertheless, the shift from online back to in-store is apparent.

I think perhaps the following chart is worth reading to consider the consumer's spend:

Entertainment seems to be taking the biggest hit of the discretionary spending squeeze.

Switching to the US now, another chart stood out:

That is 14.93% for CCC rated paper!

This isn’t as bad as it looks in a wider historical context:

But still suggests a significant tightening of lending to “junk” companies.

Small Caps

System1 (SYS1.L) - Results & Q1 Trading & Buyback

Rather strangely, we got three RNSs released at the same time from System 1 on Tuesday. First up, they announce a new share buyback program:

£1.5m is a lot for an illiquid stock. Then we get results for the year to 31st March:

These are very poor results, but we knew they were going to be poor since the shares almost halved on a profit warning. The shares had been recovering somewhat, though, helped by the announcement of a £1.5m tender offer last month with details promised to follow.

Then we got a Q1 trading statement where we find out the share buyback is taken off the tender offer amount:

The tender offer will seek to return the balance of the £1.5m, after deducting the value of shares bought back on market from today until the announcement of the tender offer.

Why we needed three separate RNSs issued at the same time to get the full picture, we don't know. It is a good job that this company isn't in the business of improving communications, right?!

Like the results, the Q1 trading update itself is also poor:

Revenue in Q1 declined 20% on the comparable period last year to £5.2m, and Data products accounted for £2.9m, representing 57% of the quarter's revenue, the highest absolute and relative quarterly performance for our automated predictions since launch in 2020. Compared with the previous quarter, total revenue was 1% lower and Data revenue grew by 21%.

Data products are doing ok, but the rest of the business seems to be really struggling. And, of course, data products on their own get nowhere near covering the admin costs. In the current inflationary environment, these trends could easily see this slip into losses in the coming year. The forecasts of £28m revenue & £1.7m PAT surely look unachievable now? And even if they did hit these figures, they are on a forward P/E of 25.

The only bright spot in the results is the cash generation:

Again, poor communication since they don't even include a reconciliation between the Profit & Cash from Operations, so they don't show how this figure is derived! A quick glance of the balance sheet shows that it was almost all working capital flows, though, which are unlikely to be sustained. Indeed, in the Q1 trading statement:

Q1 period-end cash, net of borrowings, was £7.1m, compared with £8.7m at end-March 2022.

We get that this cash is surplus to requirements, and perhaps the larger shareholders here don't want dividends for tax reasons. Still, by buying back shares at such a high rating (they were even buying them back above £4/share), they are likely to be destroying long-term shareholder value.

The other reason they may be taking this course of action is to hold up the share price. This is perhaps why the shares were slow to react to this poor trading. These things are rarely effective for long, though, as we have seen many times in the current market; as soon as the buyback ends, the share price collapses anyway.

Hostmore (MORE.L) - Trading Update

An inline trading statement from the strangely named Hostmore:

Guidance for the full year remains unchanged, with LFL revenues for the period since 23 May 2022 in line with the expectations set out in the trading update issued on 26 May 2022.

CEO Robert Cook seems to think he’s running a charity, though:

I am grateful to all our valued and loyal customers for their ongoing support despite the financial challenges currently faced by consumers.

“Giving just £5 will get you a small bowl of chips, £20 will buy a whole main course (no sides). Please give all you can to support this great cause!”

This part is very positive, though:

On 5 July 2022, the Group extended its primary banking facilities for an additional 12 months to 1 October 2024. The terms include an increase in the value of the Revolving Credit Facility to £30m from £25m in support of the Group's capital allocation policy.

Apparently, their lenders have a very different view of the risks to the business than equity investors right now, although we don't know whether their interest margin was increased. Potentially many of the institutions that never wanted these shares in the first place sold out on or before the 30th of June. Since then, the share price has shown some strength, and a PE of 5x for a business that is trading inline in difficult conditions and has apparently turned the corner on reviews/customer experience looks too cheap to Leo.

Creightons (CRL.L) - Preliminary Results

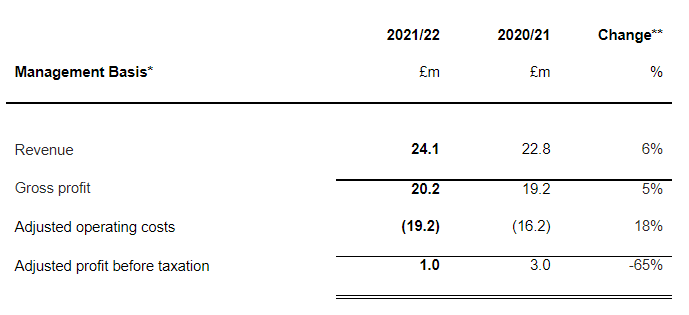

Revenue from core business excluding hygiene and acquisitions increased by £10.3m (21.8%) to £57.3m (2021: £47.0m).

This is somewhat behind what we were hoping for, with a knock-on effect to the bottom line. The two issues are Private Label and Brodie & Stone. On the former, the path isn't always smooth, but all things being equal incremental growth in H2 over H1 is normal, but this year it was 10% down. Brodie & Stone badly underperformed Leo’s expectations with just £1.3m in H2 compared to £5.8m FY 2020 (pre-acquisition). These issues could be caused by retailers stocking early for Christmas over supply chain concerns, though.

They have acquisition aspirations, but the relatively low share price is a problem. As is that, they have to make up deferred consideration for Emma Hardie up to the equivalent of a 125p share price. The current cost of this is around 2p a share in cash, so not that significant.

Here's another way of raising the cash:

The Directors do not propose a final dividend for the year ended 31 March 2022 (2021: 0.50p per ordinary share).

But investors may think cash is a problem in general:

The Group acquired 2 brands during the year with a total cash outflow of £8.9m, these acquisitions were funded using cash resources and bank facilities. Net cash on hand (cash and cash equivalents less short-term element of obligations under finance leases and borrowings) is negative £2.1m (2021: positive £6.2m). The reduction in cash is mainly attributable to business acquisitions and related increase in working capital. The Group generated £2.0m (2021: £6.2m) from operating activities.

Here's their reason for not paying a dividend:

The Directors do not propose a final dividend for the year ended 31 March 2022, (2021: 0.50 pence per ordinary share) due to the challenging and volatile economic conditions facing the Group and the need to be prudent about utilisation of cash resources. This is consistent with the directors' objective to align future dividend payments to the future underlying earnings and cash requirements of the business. The total dividend paid for the year ended 31 March 2022 is 0.15 pence (2021: 0.65 pence).

If you read that carefully, it looks like both a profits and cash warning for the current year. There is the usual stuff about the supply chain, and it is easy to make the mistake of tuning it out.

These pressures have manifested in the form of delayed deliveries from suppliers, higher input, energy and overhead costs. These pressures are expected to continue.

Accordingly, we have embarked on a programme of overhead cost reduction and of improving manufacturing efficiencies…

Many companies and individuals will be doing this right now. Looks like the previously stated "aspirations" are out of the window?

We are still keen to expand but will only do so when the infrastructure is fully repositioned to deal with the volatile conditions we are facing.

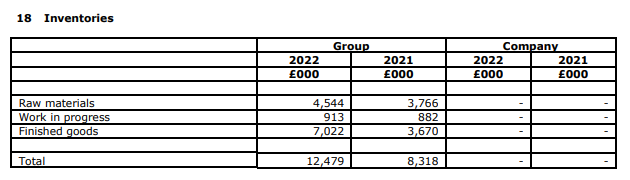

In some ways, it is reassuring they have not charged on as before. But perhaps the most worrying part is the inventory build. Inventories are up to £12.479m from £8.318m. £1.648m [restated in these results as £1.646] was taken on from acquisitions. Ex-acquisitions, inventories are therefore up 30% YoY, and that assumes they have not yet been able to normalise Emma Hardie. The annual report also shows a short to finished goods:

This suggests a recent slowdown in sales and likely further writedowns. We do not buy the idea that supply chain issue mitigation could cause such a movement alone.

The historical P/E is now below 10. The company has always been operationally good, so we expect them to be able to deal with these problems in time. So this could be a good entry point for those who believe the long-term story remains intact. Given the lack of forecasts and risk of further inventory write-downs, this will only attract the most patient of investors.

Appreciate (APP.L) - CEO Resignation

The share price reacted by dropping 11% on this announcement which does seem a little harsh for a CEO resigning after 3 years of service. Given that thy also lost their CFO recently and only appointed an internal interim CFO, the risk is that this may have been the result of a strategy disagreement leading to a boardroom bust-up. If so, then there will be a lot of uncertainty going forward.

On Friday, the company announced two non-exec director buys. However, they look relatively small in monetary amounts and coordinated, which says more about what they want you to think rather than what is actually going on. Still, a buy is definitely better than a sell or further resignation.

Mpac (MPAC.L) - Trading Update

Revenue is in line, but profit is significantly below expectations due to the impact of inflation plus the supply chain issues.

Leo had been looking into Mpac in detail on his blog. He was expecting updates on three things: 1) a revenue beat due to a strong starting order book 2) bad news on the pension deficit payments due to the valuation date 3) hopefully some update on FREYR. Instead, we got a massive profits warning. Their broker Equity Development say:

FY22E EBITDA (adj.) of £6.1m, reduced from an estimated £11.6m.

This means that Mpac will fall into a FY loss by any reasonable measure (e.g. their "one-off" costs continue at the same level indefinitely). Forecasts are for a return to profit in 2023, but on the adjusted EPS basis, forecasts are down from 41.0p to 21.6p. That's more than a halving on any reasonable basis. Full recovery is not expected until 2024.

The primary hit is on the cost of sales, with gross margin expected to fall from 30% to 25%. And they expect these to remain weak in 2023. The obvious response to some of these challenges is to accelerate the move to more modern components that aren't necessarily usefully better at the job but which have better availability and lower cost. This may require R&D spend impacting cash.

In the meantime, the Group has been proactive in implementing mitigation measures which include securing alternative sources of electronic component supply, increased focus on reliable planning data from our recently implemented ERP system, close management of our supply chain and implementing cost savings initiatives.

Looks like they are going to muddle along, concluding:

Beyond these short-term operational challenges, the longer-term outlook for the business remains positive. We carry forward a prospect pipeline and order book, concentrated on companies in our core, resilient, end markets of Healthcare and Food and Beverage and the balance sheet remains strong providing us with the ability to invest in the Group for growth over the medium term and beyond.

That's a good reminder of the medium-term strengths of the business, but it adds nothing new. So what about the valuation now? The unfortunate truth is that problems like this tend to go on for longer than most expect. But by forecasting no recovery until FY24, this builds in scope for that, and they could design out electronic components in short supply, and we would expect them to be more agile than most.

FY 2024 adjusted EPS forecast is for 41.6p. After pension payments and costs, that is more like 22p. So, far in the future, and given the uneven history of profitability, the current buy price of 240p makes little sense on that basis. We do believe that potential further FREYR contracts have significant option value, but the risk of this going to a competitor must now have increased. Perhaps a wait and see approach is the best?

Joules (JOUL.L) - Response to Media Reporting

We hadn’t spotted The Times article over the weekend, but given that they give a detailed breakdown of their current balance sheet, we knew it would be along the lines of the recent AO article. Here’s that breakdown:

The Group confirms it has appointed KPMG debt advisory to assist in this process. As at 29 May, the Group had net debt of £21.4m, giving £11.3m headroom within its banking facilities, in line with the Board's expectations. Whilst the Group continues to manage its cash resources carefully over its seasonal borrowing peak, it expects to have sufficient liquidity to manage its working capital requirements over this time.

The retail gazette also ran with the story:

According to the title, consultants from KPMG’s debt advisory practice are said to be exploring options, including raising fresh capital, after inflationary pressures drained the retailer’s cash reserves.

The company seem to think they won’t require fresh equity capital, but, of course, they need to say that to be able to raise fresh capital in the current markets, so we don’t think we can rule out a heavily discounted placing a la AO. The share price reaction certainly said that the market agrees with this assertion.

Portmerion (PMP.L) - Trading Update

When Mark visited Portmerion (the village) over the Jubilee weekend, there was a thunderstorm in the background. This week the storms continue to rumble in the distance:

With consumers facing increasing cost of living inflationary pressures, together with the impact of the Ukraine war on raw material prices, global supply chain issues and weaker sales markets, we remain cautious as we enter the key second half trading period.

In particular, they say "weaker sales markets", not "the potential for weaker sales markets". So perhaps they are already being hit by the odd incongruously large raindrop. But of course, like every other business, they expect to outperform:

The benefit of our diversified sales markets, strong brands and the ongoing strategic investment in productivity, automation and efficiency has mitigated much of the increasingly challenging market conditions and input cost inflation during H1.

However, we think this last sentence tips this firmly into profits warning territory:

However, we have also seen retail customers react to the economic environment by de-stocking in the first half and we remain cautious to the risk of further declines in consumer and retailer confidence for our key second half trading period.

By "retail customers", we take it they mean "retailer customers". Speaking for ourselves, none of us have been destocking on plates!

Their broker, Singer, have updated with some good analysis:

a solid 5% y/y growth. A pleasing outcome in our view given the soft consumer backdrop and a very stiff 35% comp. Notably, given the position after four months was 2%, this implies an acceleration towards 10% over May-June.

We make no forecast changes at this juncture, opting to wait until the September interims when management will have much better visibility on the H2 order-book / outlook. To hit our full year sales estimate of £110.2m, Portmeirion will have to grow sales by 3.2% in H2. For reference, our sensitivity analysis shows a 4% impact on PBT from a 1% sales change

When they commented on the AGM update, Singer were teeing up a downgrade to accompany the H1 TU. Now Singer are teeing up a downgrade to accompany the interims. We expect it will probably come, although the market has been doing a lot of anticipating lately. The question is if it has now anticipated too much?

Sanderson Design Group (SDG.L) - AGM Trading Update

A fairly short trading statement this week that starts with:

Overall, trading at the Company in the financial year to date is broadly in line with the same period last year and profits remain on track to meet the Board's full year expectations.

So in-line overall, but given that Stockopedia had revenue forecast to grow this year, we are not sure the market is going to like the word “broadly” in there. Which, of course, means slightly below. This bit sounds positive:

The key growth trends outlined in our full year results on 28 April 2022 - including manufacturing, the Morris & Co. brand and the US - have continued strongly in the weeks following the results announcement. Licensing has also continued to perform well.

But the lack of any actual figures being provided five months into their trading year means we don’t really have much idea. Given the level of uncertainty in the consumer market, perhaps they have no idea either!

Vianet (VNET) - AGM Statement

The focus starts with things not having gotten worse:

I am pleased to report that the good revenue momentum experienced by the Group at the back end of last year has continued into the new financial year with recurring revenues remaining strong at c. 85%, with accompanying gross margins being maintained across the whole business.

Vianet's statements can be overly optimistic, at times, making this relatively downbeat for them. This is what they say on Vending:

Specifically in Smart Machines, primarily as a result of our commercial focus on exciting opportunities for our telemetry, SmartVend software and award-winning contactless payment solutions, we are seeing excellent customer engagement and encouraging recurring income growth in this division.

Customer engagement => expressions of interest => order book => sales / receivables => cash. Which is quite a long chain. And the recurring revenue aspect spreads the cash out over many years. So shareholders may not share their excitement yet.

On the pub side, they are materially ahead on revenue. And with fewer pubs than pre-pandemic, it is an achievement to be getting close to pre-pandemic sales. Inflation helps here, which seems to be running at around 50% in the pub sector. The question is whether they have been hit by supply chain problems or not?. Some, like auto OEMs, got hit pretty much on day one but then have profited from the tacit agreement across their peers to respond by raising prices rather than work around problems. So this is good news:

Whilst global semi-conductor supply shortages are resulting in higher hardware costs, we are actively seeking to recoup these additional costs wherever customer terms allow. However, our overriding commercial imperative is to keep the sales pipeline flowing to expand the Group's installation footprint and grow top line sales.

There is no broker update, and there does seem to be a margin warning in there, but it only affects the hardware installation side, which is presumably less than 15% of the non-recurring revenues. The forward P/E of around 19 looks expensive in the current market, though.

That’s all for this week. Enjoy the summer sun!