Small Caps Live Weekly Summary

CMCX DSM NWOR SNX MIND SCE TMG

Another fairly quiet week for news. However, some UK small caps have been anything but quiet, with several share prices in companies we follow gaining or losing 10% or more on no news. It may simply be short-term momentum traders and illiquid markets or concerns amongst some about the tax plans for the incoming Labour government. Whatever is causing these moves, they often quickly reverse, so they can provide some great opportunities for the quick-reacting investor. Here’s some of the news we looked at this week:

CMC Markets (CMCX.L) - Final Results

While some investment in IT has borne fruit, they highlight a particular issue with the UK Invest platform that a few SCLers were looking forward to being customers of, but which was repeatedly delayed and was eventually launched as a little more than a toy:

…a non-recurring £12.3 million impairment charge relating to internally-developed platforms for the UK Invest and cash equities offerings

Much of the other poor investment we previously commented on wasn't capitalised, but sacking staff costs money either way:

£4.3 million of one-off costs relating to actions to reduce global headcount

There risk was that, such was the chaos at times, liquidity and gross exposure control may have been compromised. Perhaps this is an admission that systems here weren't as good as they could be and is (as far as words can be) reassuring:

...the launch of our global Treasury Management System focused on efficient cash management, currency and liquidity optimisation.

Despite the problems, Invest UK is mentioned in the operational highlights, but the success has clearly come in B2B. Where they have made good progress is in growing their B2B leveraged trading side – B2B net trading revenue share has increased from 11% in FY2020 to 22% in FY2023. Further launches to come mean that momentum may have further to run, even in current market conditions. This week, they say:

· CMC Markets Connect brand, API ecosystem and world-leading financial markets technology continues to underpin our growth and has proven critical in growing our B2B and institutional offering with several major client wins during the year and a strong pipeline of potential clients.

· Significantly bolstered product suite with the rollout of options and addition of cash equities to our institutional offering, to expand this valuable segment.

There is clear signalling over the future direction:

Institutional, B2B and multi-asset, multi-currency platforms, across all brands is the future, and ours.

There's no analyst coverage available to us, so it is difficult to compare results and outlook to expectations, but here's CMC's own curated analyst summary:

Note only 5/6 analysts were included because one was stale, and no trading updates have been issued since March, so the April collation should be current. These are the actual results:

So, NOI is a beat of 5%, expanding to 13% at the PBT level and 20% at the EPS level. And that is even assuming the forecasts were for the lower, unadjusted figures.

As to outlook:

Management is guiding to net operating income of between £320-360 million in FY25 on a cost base, excluding variable remuneration and non-recurring charges, of approximately £225 million.

That is well ahead of forecasts (or at least those from April). Comparing to FY 2024 and applying the cost base saving of £25m (less a bit of increased variable compensation) and assuming the exceptionals don't recur, we could easily be looking at PBT of £100m even at the bottom end of the NOI range. At the mid-top end, £120m looks possible. EPS forecasts similarly look way off, with 25p the current baseline.

Accordingly, the share price strength seems justified, though investors need to remember that earnings are volatile here, and a current forward P/E of over 10 is only justified by earnings momentum.

Downing Strategic Microcap Fund (DSM.L) - Dividend, Requisition Notice & Asset Sales

We follow this company not so much as an investment itself but because it is liquidating its portfolio of largely undervalued and illiquid small cap shares. Firstly this week, we got an intraday dividend announcement, with an ex-date earlier than expected, for more than originally signalled, with no declared pay date of 18th July and, most importantly, a proposal to then bring in liquidators.

Then, a second statement explaining why: Milkwood are trying to block any form of asset return to maximise the rump they think they can control. The dividend pay date is, barring a possible injunction, well before any general meeting can take place.

The rump after the third dividend will likely be so small that Milkwood could easily take control via a bid if they were determined, but it might no longer be worth it for them. Meanwhile, liquidation could mean a fire sale of other assets and could present opportunities.

One of these will no longer be National World, as Downing announced this week that they had sold all the shares. This explains the share price weakness earlier in the week, and then, with the market deducing this overhang had cleared, the shares rose slightly. Trading on a P/E of around 4 after adjusting for the net cash, this still looks materially undervalued.

Having held off selling until now, from trade watching, we deduce that they used the liquidity from a contract win announced at Synetics to sell down here. They look to be around halfway done here, and when they are out, this is also one that looks good value - the P/E is around 12, but it now looks likely they will beat current EPS forecasts. Just not as good value as National World since the share price at Synetics has doubled in the last six months. There is also a small issue of management trust - they were pretty evasive during their recent legal worries, which may put some investors off.

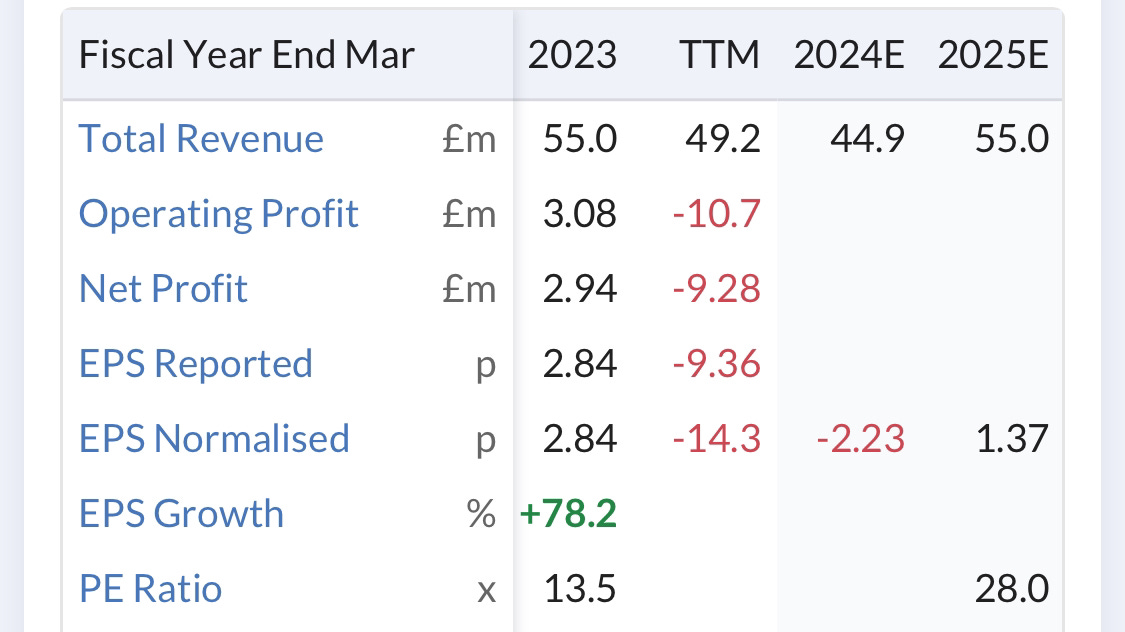

Mind Gym (MIND.L) - Final Results

These results look really poor:

And it sounds like a long road to recovery, too:

· FY25 will be a year of recalibration as we implement the new strategy which will return MindGym to its historic performance levels

· Whilst it will take time before the full benefit of this new strategy is realised, the Board expects EBITDA profitability and cash generation in FY25

EBITDA profitability, of course, means loss-making. So this looks like a further miss if these forecasts are up to date:

The market cap is now less than 1x sales so this may be good value if they eventually hit their target EBITDA margins. But then there are better businesses out there on cheaper ratings that don’t require a far-off recovery. And £1.4m cash and £2m facilities don’t give a lot of headroom versus £40m revenue for any further deterioration in trading or adverse working capital flows. So, the risk has increased significantly here, too.

Surface Transforms (SCE.L) - FY23 Audit Update

Any RNS with this title is not going to be good news, and this is no exception:

There are two particular areas that have and are contributing to the extended audit timeline:

(1) Impairments to the carrying value of certain intangible and tangible assets; and

(2) Revenue recognition, namely relating to revenue generated from engineering, testing and tooling services provided to OEM customers during the development phase of the contract.

Although the impairments are non-cash, writing off a furnace surely means they need to spend more cash in the future when they want to scale production. There doesn’t seem to be any indication that they are pursuingg the supplier of the costs. The only reasons we can think of why this may be the case are:

a) they didn’t get the specification right; or

b) they agreed to terrible commercial terms with no need for a supplier to rectify an underperforming contract; or

c) they are in such a weak position they don’t think they can enforce their contract; or

d) the supplier went bust.

Surely they would have told us if it was due to supplier insolvency, which makes this uninvestable because who knows what else they have badly contracted and leaves them exposed to unknown future losses.

Mission Group (TMG.L) - AGM Trading Statement

Having rejected a tie-up with Brave Bison, the pressure is on the management here to deliver as a stand-alone group. So this is a good start:

Trading in the Period has continued in line with the Board's expectations.

With cost savings starting to come through:

The Group has delivered good progress against the Value Restoration Plan announced on 17 January 2024, with the vast majority of the £5.0m of annualised projected profit improvements already secured for the year. The initial phase of this involved significant one-off headcount reductions completed late in 2023, equating to c£2m of annualised costs savings. The second phase of this involves £3m from a combination of cost savings and profit improvements through efficiency gains. Most of the cost savings have been implemented, the operating efficiency improvements are tracking to expectations and are expected to be fully delivered by the end of 2024.

However, they remain heavily indebted, and the banks can remain supportive for only so long. After all, there is no asset backing in this people business. Unsurprisingly, then, it sounds a lot like a raise is on the way:

As previously announced, the Group continues to progress discussions regarding options to deleverage the Group's balance sheet, alongside the successful refinancing of the existing debt facility with long-standing lender NatWest, announced on 28 March 2024. A further update will be provided when appropriate.

It would seem folly to consider investing here until it is clear that they can sufficiently deleverage and at what price they can get the raise away at.

That’s it for this week. Have a great weekend. It looks like summer may have finally arrived in the UK!