Small Caps Live Weekly Summary

GMS JSE MRK PRES SDG THRU WYN

After a bit of a lull, lots of small cap news appeared this week. Unfortunately, it arrived at the same time as the British summer. Given that this is often fleeting at best, this has somewhat dulled the appetite for detailed share discussions. Here is what we managed to get done from the sun lounger!

Gulf Marine Services (GMS.L) - Secondary Placing

This is not a placing by the company but one by major shareholder Seafox:

…a 28.5 per cent. shareholder in GMS to sell approximately $10 million of ordinary shares of 2 pence each in GMS ("Ordinary Shares") (the "Placing Shares") at a minimum of 17 pence per Ordinary Share (the "Placing").

They got $11m away but at 17p, which suggests they were/are fairly keen sellers, but that demand was there at that level too:

Zeus announces that the Selling Shareholder has sold in total 51,136,347 Ordinary Shares (the "Placing Shares"), representing 4.8 per cent. of the issued share capital of GMS, and equating to c.$11 million. The Placing Shares were placed at a price of 17 pence per Placing Share…

Normally, such holders agree not to sell for another 6 months to a year. However:

Following the Placing, Seafox will hold 253,686,385 Ordinary Shares equivalent to 23.7 per cent. of GMS's issued share capital. Seafox has undertaken to Zeus that it will not, for a period of 75 days from 30 June 2024, dispose of any further Ordinary Share

75 days is much shorter than is usual. So, with 23% still held, we can see this as an overhang on the share price for quite some time to come.

Jadestone Energy (JSE.L) - First Gas at Akatara

Akatara commissioning continues to go smoothly and on time:

On 22 June 2024, reservoir gas was introduced to the Facility from the Akatara-A4 well, and a period of final commissioning using reservoir gas has now commenced. Condensate is already being processed to the Facility's storage tanks in preparation for sale, with first commercial gas and LPG sales to follow.

It seems the market has been wrong to read across the issues at Montara to their general ability to execute complex Oil & Gas projects. It seems likely this will gradually be reflected in a higher share price as the doubts over their execution ability subside and the cash flow from Akatara accumulates.

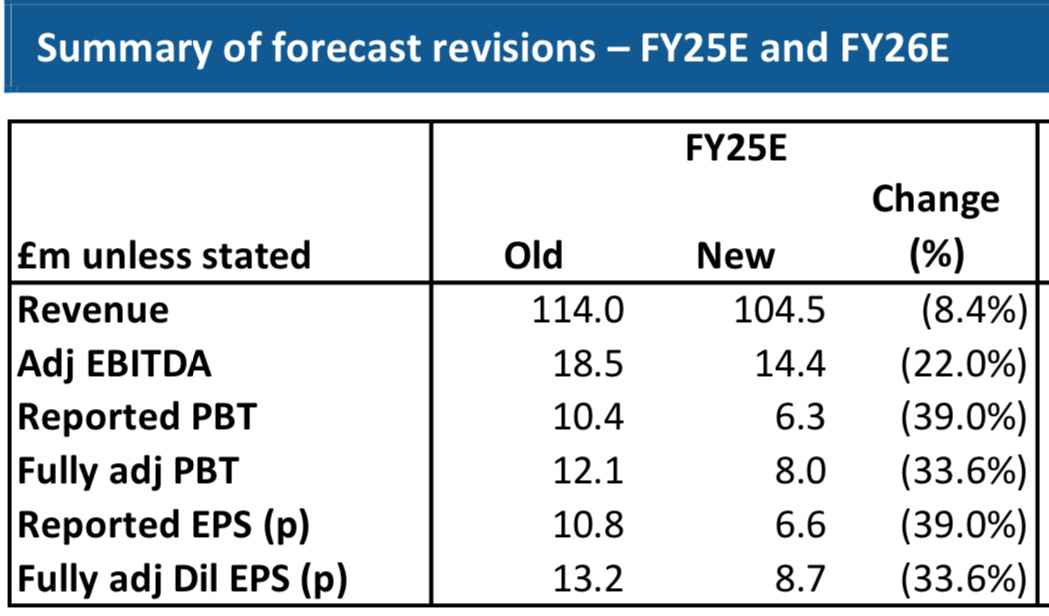

Marks Electrical (MRK.L) - Final Results

The weak bottom-line performance here was already known, although it is never nice to see EPS halve:

· Record full-year revenue of £114.3m (FY23: £97.8m) up 16.9% year on year, doubling the revenue we achieved in the year prior to listing (FY21: £56.0m).

· Adjusted EBITDA(1) of £5.0m (FY23 £7.5m) in line as previously guided, maintaining strong cost control despite downward margin pressure as a result of consumers trading-down, and continuing our strategy of gaining market share profitably.

· Adjusted EPS of 2.45p(3) (FY23 4.82p), statutory EPS of 0.41p (FY23 4.91p).

The outlook is better, though:

Strong trading performance in April, May and June, with double-digit revenue growth and momentum starting to pick-up following the weaker January to March trading period, providing us with optimism for the year ahead.

However, no hope of margin recovery in the short term, with only some hopes for the medium term on the cost side from leaving Euronics:

...which we anticipate will lead to revenue and margin upside in the medium-term

How much runway?

growing our share from 2.5% to 2.8% of the overall Major Domestic Appliances ("MDA") market and from 4.7% to 5.3% in the online segment

Marks has been going after market share, but the problem this year was lower value per van driven by mix rather than volumes. The question remains whether it is structural due to the new cohort of customers or temporary due to affordability pressures.

Canaccord says "No changes to estimates", which isn't entirely true, but perhaps close enough. EPS of 3.5p for FY 3/2025 is forecast.

Market leader AO, which claims to be the UK market leader in Major Domestic Appliances with a 15% total market share, is following the opposite strategy. Their revenue is down, but their margin is up. So far, the market has much preferred AO’s strategy with much better recent share price performance. With both companies on similar ratings, the jury is out as to which strategy will prove the right one.

Pressure Technologies (PRES.L) - Interim Results

Poor results, with slightly increased revenue but declining margins and increased loss:

● Group revenue of £15.0 million (2023: £13.8 million)

● Gross profit of £3.2 million at 22% margin (2023: £3.7 million at 27% margin)

● Adjusted EBITDA1 of £0.1 million (2023: EBITDA of £0.3 million)

● Adjusted operating loss2 of £0.7 million (2023: loss of £0.5 million)

● Reported loss before tax of £1.2 million (2023: loss of £1.4 million)

● Reported basic loss per share of 3.2p (2023: loss per share of 3.9p) and Adjusted basic loss per share3 of 2.7p (2023: loss per share of 2.3p)

● Net debt4 of £3.3 million (2023: £3.7 million; 30 September 2023: £2.4 million); Net borrowings, excluding asset finance and right of use asset lease liabilities, of £0.9 million (2023: £0.9 million; 30 September 2023: £nil)

The order book declines as well:

Order intake of £16.6 million for the 26 weeks ended March 2024 (2023: £29.3 million, including major UK naval order of £18.2 million) supports a current order book of £21.9 million at March 2024 (2023: £25.7 million).

They appear to be selling the only part of the business that has increased sales, margins and order book:

PMC revenue in the first half of FY24 increased by 73% to £8.5 million (2023: £4.9 million), reflecting growth in the oil and gas market and strong operational performance, supporting consistent delivery against customer commitments.

By contrast, the bit they are keeping:

However, a shortfall in CSC performance is expected for the full-year, driven by the deferral of a portion of UK defence contract revenues to future years and operational delays in the first half, further impacted by delayed order placement for new hydrogen storage contracts due to the UK general election, now expected later in FY24.

They are betting their future on:

Recent announcements of significant funding from UK Government to support the development of new hydrogen production, storage and distribution hubs across the country provide significant opportunities for CSC in the supply of new hydrogen storage and transportation systems for refuelling and decarbonisation applications.

This looks highly speculative at this stage.

The notes reveal that they expect a better H2 with:

Order books in CSC and PMC underpin the outlook of the Group in the second half of FY24. Given the current divisional trends and performance outlook, the Board expects the Group's full-year FY24* Adjusted EBITDA to be not less than £1.0 million.

However, that is almost certainly an accounting loss, even on an adjusted basis. And it is not clear how much of this is due to the performing part of the business that they are selling:

FY24 outlook includes CSC and PMC, on the basis that PMC is not sold in FY24 and remains a continuing operation

Even the rather modest 1p EPS forecast now looks dead. Even more so if PMC is sold.

Sanderson Design (SDG.L) - Trading Update

A big profits warning here:

As a result of this trading performance, the Board expects Group trading in the current financial year to be below its earlier expectations. Underlying profits before tax for the year ended 31 January 2025 are now expected to be in the region of £8 million.

Progressive take 40% out of EPS and assume a dividend cut, too:

The blame is squarely put at UK Brand Sales:

For the first 22 weeks of the current financial year, total brand product sales were down 9% compared with the same period last year. In the UK, brand product sales were down 14%, reflecting the worsening of market conditions.

The shortfall in revenue has a particular impact on profitability in the current financial year owing to the previously communicated inflationary pressures that the business is absorbing.

The rest of the business is mostly performing in line. The big question is if this is specific to Sanderson, hoping that their markets would recover or the start of many profit warnings for housing-related stocks. Although they don’t mention it, it may not be a coincidence that the badly affected months of May and June are during the unexpected UK election period. Nor can it be ruled out that the typical Sanderson customer may be the demographic that is going to bear the brunt of any upcoming tax rises.

Progressive also cut its 2025 EPS Forecasts by about 30%, which suggests that it doesn’t see a quick fix to this situation. The share price reaction was down 20%, which, while a severe fall, certainly could have been worse. The fact they were on a P/E of c7 prior to this means that the market may already have been anticipating it somewhat. At this point, those who believe in the long-term potential of the licensing revenue will want to hang on, whereas those who think that this is another sign that the core manufacturing business is in decline will want to bail.

Thruvision (THRU.L) - Final Results

Results look pretty poor and show the risk of such high customer concentration:

Revenue of £7.8 million (2023: £12.4 million), primarily comprising Entrance Security, new Customs agency and Retail Distribution sales - reduction reflects previously announced lack of further significant orders from US Customs and Border Protection ('CBP') in 2024…

· Adjusted EBITDA loss1 was £2.5 million (2023: loss of £0.2 million), which is in line with market expectations. Operating loss was £3.0 million (2023: loss of £1.0 million).

This seems to be the key information though:

Trading in the current financial year is in line with the Board's expectations and our sales pipeline points to a return to activity levels the Group achieved in FY2023. This, coupled with the tight control over our cost base, provides us with the confidence that we are heading towards sustainable profitability and positive cashflow generation.

The "sustainable" qualifier for profitability is important, and the sales pipeline guidance is a lot more specific. A repeat of 2023 sales might lead to an EBITDA breakeven again, especially as they have value-engineered the product and outsourced some of the incremental sales effort. However, Progressive have £10.9 revenue forecast versus £12.4 in 2023, leading to an adjusted EBITDA loss of £0.8m.

On these forecasts, cash could become a concern again. We saw how large the working capital swings can be in FY 2023. Another large order near the end of FY3/2025 could leave them tight again. With year-end cash of £4.1m less the forecast EBITDA loss, and assuming a £2.1m receivables outflow, that leaves just £1.2m. Of course, the only customer capable of making such a large order is the US CBP, which would be fundable and excellent news (at least in the short term).

Wynnstay (WYN.L) - Interim Results

As widely expected, and as already flagged by the company:

Trading in April and May was ahead of the prior year and further weather-deferred sales are expected to come through in H2.

But we didn't necessarily expect this:

Group remains positioned to deliver a full year performance in line with current market expectations, with a more significant second half weighting than last year.

Of course, this is dependent on not having more bad weather. This is the risk of a second-half weighting.

It shouldn't have been this way, though. An acquisition was supposedly pretty imminent when the long-time CEO Gareth Davies had to take a leave of absence in February. Whether as a result or for other reasons, it has not proceeded. As they have cash to spend any acquisition would almost certainly have covered up any trading weakness and put them ahead of expectations. No mention of either Gareth or the acquisition pipeline is made in today's statement or the broker note. However, there is a soft downgrade from Shore:

Adj. dil EPS reduced by 1% and 2% respectively due to a higher number of dilutive shares

DPS reduced by c.3% to reflect a more prudent approach given trading conditions

This is a steady but cyclical stock and investors can do well by trading these dynamics. This is in the middle to lower part of that range on share price. However, a forward P/E of 13 is at the upper end of its typical valuation range:

As such, it doesn’t seem worth bearing the risk of a dreaded second-half weighting.

I read your posts religiously every week and every week I learn something. Thanks for generously sharing your insights!