Small Caps Live Weekly Summary

Happy Easter! AIEA GEBT HEIQ LUCE NXQ PMP QTX QUIZ ZOO

Happy Easter everyone! Hope you manage to get a restful time away from the markets for a few days. This week was another busy one, with UK companies that have a half-year end on 31st December having to report unaudited results by the end of this trading week or facing suspension. Unsurprisingly, those who left it this late were unlikely to be reporting an ahead statement. Here’s some of what we discussed this week:

Airea (AIEA.L) - Final Results

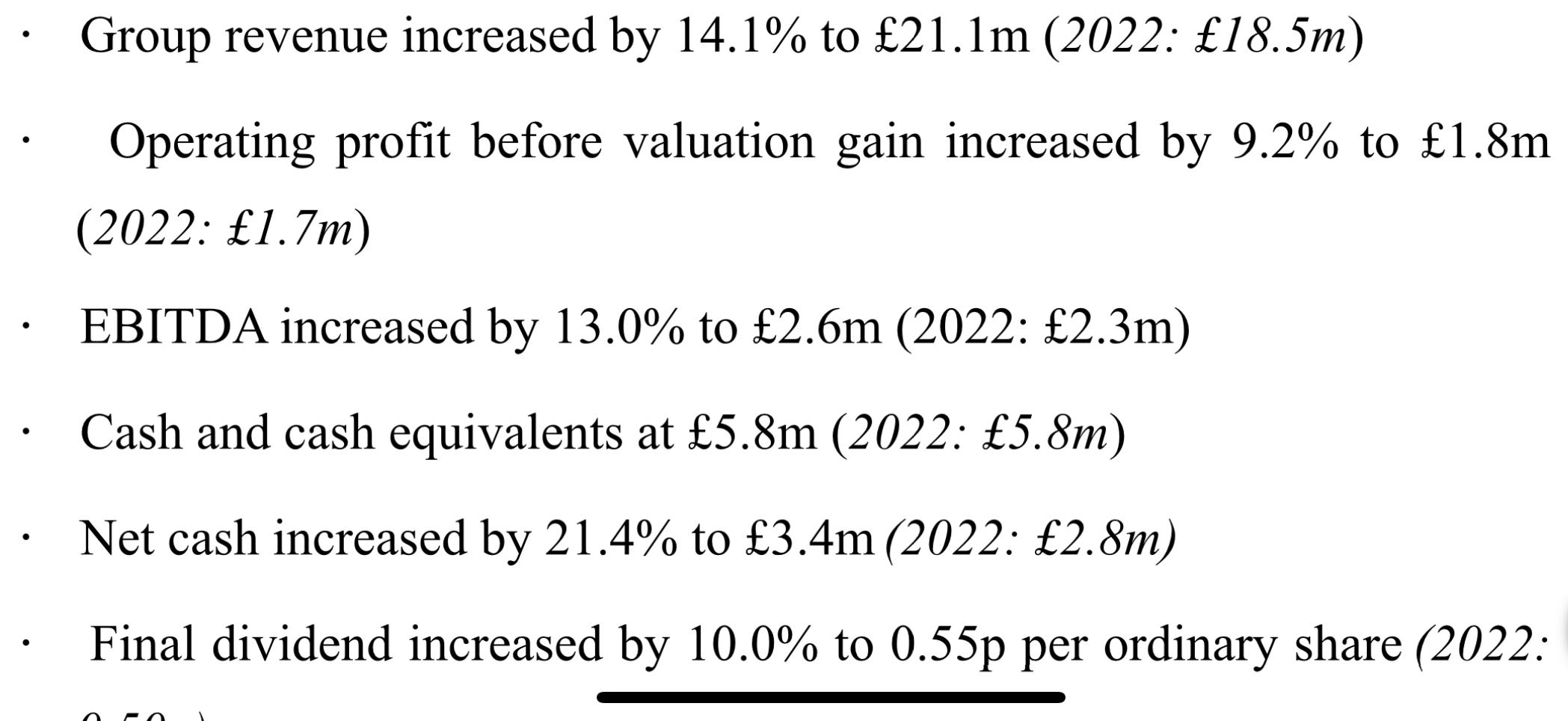

This carpet tile manufacturer has shown some decent revenue growth given the market backdrop:

The lack of operational gearing stands out, though. As they say they have invested in headcount to support growth. This leaves Mark a little disappointed. There are no market forecasts here, so investors have to do their own modelling. Mark had expected 2.7p EPS, so 1.99p is a big miss, and unless operational gearing does kick in, then the the P/E doesn’t look an obvious bargain any more as the share price has risen somewhat.

However, they have reasonable start to the current year:

"Despite the current challenging economic conditions, we are pleased to report the Group has experienced a good start to the year. Demand remains high for our carbon-neutral and low-carbon products, and we are confident of continuing to outperform the market through 2024."

Although given that they are investing significantly in new equipment, the demand must be there for this strategy to pay off. “Build it and they will come” has always been a bit hit and miss for small companies:

The Group's £5.0m investment in its manufacturing facility will substantially increase capacity and include the automation of certain processes using the latest cutting-edge Artificial Intelligence imagery and inspection technology. This investment will provide greater stability to the Group and help to deliver a period of sustained profitable growth.

There is £4.6m net cash and £4m of investment property, so they should be able to fund this, and it could be argued that it is good that they are not just sitting on the cash. However, the Pension Deficit that seemed to be largely killed off has reared its ugly head again. This sounds like a badly run scheme, too:

The deficit on the defined benefit pension scheme increased from £1.3m to £5.0m. The Group's contributions to the scheme were £nil (2022: £nil). There continues to be volatility in global equity markets with the scheme's investment strategy constantly under review to mitigate its long-term risk profile as much as possible. The Company will engage with the scheme's trustees to agree on a reasonable and affordable recovery plan. A further update will be provided at the announcement of the interim results.

Sounds like the days of nil contributions are about to end. So that is effectively a £3.7m increase in “debt” that has just appeared. The market has been pretty sanguine about this, with the price rising in response. We are just not sure why.

GetBusy (GETB.L) - Final Results

Getbusy always seem one step away from sustainable profitability. Prior to these results, broker Cavendish was forecasting 1.1p EPS, so the 0.5p delivered are a big miss. Not only that, but the unadjusted figures are still loss-making after being positive in 2022:

Cavendish are forecasting a further deterioration to 0.1p in 2024, but these results don’t give a lot of confidence that they will even hit that. As such, their £32m market cap looks increasingly out of place. Their vain search for some productivity software that may improve their results continues…

Heiq (HEIQ.L) - Interim Results

Surely these three things together won’t end well for shareholders:

Operating loss of US$11.6 million (12 months to 31 December 2022: loss of US$29.2 million)

Cash at 31 December 2023 of US$9.7 million with net debt (including lease liabilities) of US$10 million

Successful fundraising of £2.4 million through placing, convertible loan note and retail offer.

No real outlook on trading, just general platitudes. It also looks like a Freudian slip here:

With resilience, innovation, and collaboration, we are confident in our ability to raise again and overcome obstacles and emerge stronger from these testing times.

Normally, failing companies would be confident to rise again. However, Heiq says they are confident to “raise” again. If these results are any guide, they will need to raise again to avoid insolvency.

Luceco (LUCE.L) - Final Results

Luceco delivers results at the upper end of the expectations range:

2023 results at the upper end of market expectations:

o Revenue: up 1.3% to £209.0m and like for like revenue up 1.7% versus the prior year

o Adjusted operating profit: up 9.1% to £24.0m reflecting a return to strong gross margins, with overall Adjusted operating margin up 80 basis points to 11.5%

o Adjusted EPS: 11.1p - equal to the prior year due to higher UK tax impact

Although EPS is flat due to the increased UK tax rate. It looks a decent beat, although Stockopedia historical figures don’t match, so perhaps hard to say for definite:

The net debt ratio was known, but getting the explicit value demonstrates the flexibility they have for further M&A:

A further year of cash generation, driven by organic growth in addition to synergy creation from previous acquisitions, means we end the year with Covenant Net Debt of £18.4m. With the right foundations for a successful "buy and build" strategy, we continue to explore M&A opportunities that have a strong strategic fit and the potential to deliver future growth.

In the last trading statement, they beat expectations, and the share price fell from £1.50 to £1.20 over a few weeks. A further beat here sees the share price rise slightly back to the £1.30 level, which suggests that the market is struggling to value this. For us, this is an exceptionally well-run business with a decent runway of organic and inorganic growth ahead of it, and at a reasonable valuation. With these qualities, it is easy to ignore the market gyrations.

Nexteq (NXQ.L) - Proposed Share Buyback

Why are they doing this? It seems they have been contacted by shareholders wanting to sell:

The Directors also believe that the Proposed Buyback Authority would provide Shareholders with the flexibility, but without any compulsion, to realise value in respect of all or some of their shareholdings and is a tax efficient method of returning surplus cash to certain Shareholders.

The Board will only proceed to make market purchases at prices which make sense for the Company and its Shareholders as a whole and intends to only do so when there is a lack of liquidity for the Ordinary Shares.

We’re pretty sure that they don't mean they will buy when there are no sellers, rather than they will buy when there is a seller with no buyers. So we don't expect the share price to be ratcheted up by this buyback. Given that there was a keen seller that took the price down close to 90p recently, perhaps they’ve learnt that even a relatively minor institutional seller can take the price down significantly. Equally, a few tip buyers can move the price the other way.

It may be that they had an acquisition opportunity that has now fallen through. The positive is that they are doing something with the cash and therefore the valuation should include the cash rather than the headline P/E of 11ish. So not expensive by any measure.

Alternatively, it may also be that H1 trading is weak, as we know they have been guided via the H2 weighting and fear the market reaction to the next trading statement. This sort of strategy has a habit of backfiring, though. It often sees companies exhausting their buybacks at high prices, and the price still goes down if they report weak short-term trading.

Portmeirion (PMP.L) - Preliminary Results

We’ve been sceptical of the adjustments this company makes in the past. And these results are no different, turning a chunky loss into a profit:

Still, even the adjusted figures have more than halved on the year before. Leading to the dividend being slashed, as we predicted:

Prudently, given the ongoing macro-economic uncertainty and the continued prioritisation of further reduction to net debt, the Board is recommending a final dividend of 2.00p (2022: 12.00p).

In addition, their diversification strategy has been failing for 50 years:

Portmeirion Botanic Garden was first launched in 1972 ... Spode Christmas Tree launched in 1938 ... Together the two ranges account for approximately 40% of sales

They directly and comprehensively address cash and borrowing facilities:

The Group has agreed debt facilities with Lloyds Bank which totalled £25.5 million at the balance sheet date. These facilities consist of a £10.0 million revolving credit facility available until February 2025, a £5.0 million overdraft and a £7.5 million trade finance facility on annual renewal cycles, and a £10 million term loan repayable by January 2025 of which £3.0 million was outstanding at the year end. Subsequent to the year end Lloyds extended the revolving credit facility agreement to September 2025

we experienced a working capital swing of around £10.0 million during the year

You'll see that the overdraft facility has reduced, but the trade finance facility has increased. The problem is the duration of the facilities:

The Directors recognise that the current bank facilities, which include both a committed revolving credit facility of £10 million available until September 2025 and an uncommitted facility element of £12.5 million available until September 2024, are all required under both a base case and downside scenario in order to provide the Group with sufficient liquidity to continue trading.

So Lloyds have a revolver pointed at their heads and:

Conclusion - Going concern assumption appropriate with a material uncertainty

This is new. No material uncertainty existed last year. In addition, the company seems highly confused whether it is preliminary or final audited and whether than annual report has been issued. It does say it is preliminary, but also:

The auditors have reported on those accounts: their reports were (i) unqualified, (ii) contained a reference to the material uncertainty in respect of going concern to which the auditors drew attention by way of emphasis without modifying their report, (iii) did not contain a statement under Sections 498(2) or (3) of the Companies Act 2006.

There is no annual report on the website, yet they say:

...the Group has prepared its annual report...

...our annual report and accounts includes...

The answer is at the very end:

Availability of annual report and accounts

The accounts for the year ended 31 December 2023 will be posted to shareholders on or before 24 April 2024 and laid before the Company at the Annual General Meeting on 21 May 2024.

If their language is accurate then the annual report has been prepared but they are holding it back, I assume because it contains bad stuff they're hoping people won't read. In any case, there is no excuse not providing any notes to the balance sheet at this stage.

This may well prove the cyclical low in trading, but given all that, it is hard to trust that the real financial performance of the business will recover anytime soon.

Quartix (QTX.L) - AGM Trading Statement & CFO Resignation

This is an in line statement, with helpfully what those expectations are compiled:

The Board believes that consensus market expectations for 2024, prior to this announcement, were as follows: Revenue £32.1m, Adjusted EBITDA £5.4m and underlying free cashflow of £3.43m (which excludes expected cash expenditure of £2.5m on the 4G upgrade programme during the year).

However, they don’t appear to be willing to share the PAT or EPS consensus, since presumably these would look rubbish and that they haven’t bounced back. In other signs that to the untrained eye these may appear rubbish is that they have sacked the CFO. She is thanked and wished well so perhaps no skeletons. However, they don’t appear to have managed to appoint a new CEO. So it looks they may have trouble getting anyone willing to take the top jobs. Given the many years with no real growth and the forward P/E of 20, you can see why people would be reluctant.

Quiz (QUIZ.L) - Board Update

This is all starting to look a bit like moving the deck chairs on the titanic. One Ramzan replaces another:

Sheraz Ramzan, current Chief Commercial Officer, has been appointed as Chief Executive Officer with immediate effect.

We just can’t believe they have wasted all that cash balance they had:

As at 27 March 2024, the Group had total liquidity headroom of £2.9 million, being a cash balance of £0.6 million and £2.3 million of undrawn bank facilities. The Group's £4.0 million of bank facilities are scheduled for renewal in June 2024.

Looks like they are going to be relinat on bank facilities that have three months to run!

Zoo Digital (ZOO.L) - Trading Update

The shares responded positively to this update:

As a result, the Company expects to beat revised market guidance for FY24* with revenues of at least $40 million.

* The Company understands market consensus for FY24 to be revenue of $37.6 million, EBITDA adjusted for share based payments loss of $14.0 million and net cash of $1.6 million.

However, looks like they are still significantly loss-making:

Consequently, the anticipated EBITDA loss will be reduced. Net cash on 31 March 2024 is expected to be at least $3 million, also higher than revised market expectations, and although the Company has no debt it intends to renew its current undrawn facilities when they fall due.

Looks like they will need those facilities to us. 2025 is looking better:

The Company's order book for FY25 Q1 is currently up by 30% on FY24 Q4. This order pipeline from major customers underpins an expectation of a strong recovery in revenues in FY25 H1. Despite the implemented cost savings which have resulted in expected Q1 direct staff costs 30% below the prior year period, the Company is well positioned to take on increased levels of business as the industry reopens.

You have to wonder why they didn't cut these costs sooner, and then they wouldn't have run the business so close to insolvency if the strike hadn't been resolved.

That’s it for this week. Have great long weekend.