Small Caps Live Weekly Summary

ALU CAPD CRL EAH RWA SOS

Hope everyone is enjoying the rare sunny weather in a British summer. Understandably, many commentators will have been focussing on having fun in the sun, but here are some of the few things we did discuss this week:

Alumasc (ALU.L) - Trading Update

Good news here:

Underlying profit before tax ('UPBT')1 now expected to be at least £12.6m, ahead of current market forecasts2 and the prior year (£11.2m)

And the market has taken it as such, bidding the shares up by around 15%. However, their broker Cavendish are relatively conservative in their quantification of the beat here:

We upgrade our FY24E expectations, with adj EPS up 4.5% to 26.1p and FY25E adj EPS by 3.1%

The magnitude of the rise is perhaps a reflection of the apparent low rating here. However, the keyword is “underlying”. This is a company that loves an adjustment, as the following chart of their exceptional costs shows:

These may be exceptional, but they are not non-recurring. As such, this week's rise may be a little excessive.

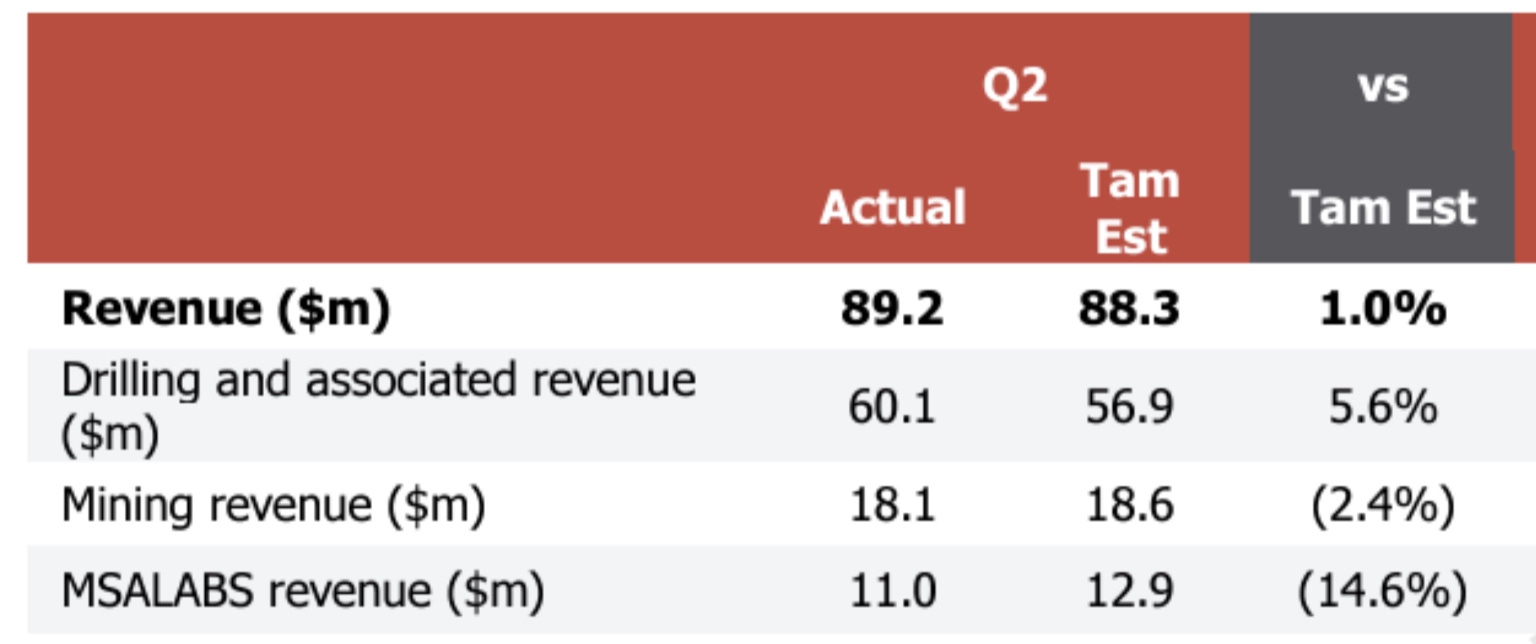

Capital Limited (CAPD.L) - Q2 Trading Update

For the first time in a number of quarters, Tamesis have them delivering ahead of expectations:

The top line was 7% beat vs. Peel Hunt, too. MSALABS installations are clearly running behind where they’d like them to be. Although in the context of historical growth rates of 50-100% CAGR

In these results, they also announce a slight extension of the Sukari waste-stripping contract. This is good from a revenue point of view, but it means they probably don’t have anything else lined up. With record gold prices and delivery delays on big yellow kit we’d still prefer they sold these at the end of the contract and used the cash for better ROCE opportunities.

Something that is definitely good news is the highest ARPOR that we can remember seeing, which will help the bottom line as well as revenue:

Average monthly revenue per operating rig ("ARPOR") was US$211,000 in Q2 2024, up 15.3% on Q2 2023 (US$183,000) and 4.5% on Q1 2024 ($202,000). This strengthening in ARPOR is primarily the result of the ramp-up of high-quality contracts, as well as a continued focus on efficiency at our more established sites.

But the utilisation is a bit below what we’d want to see. New rigs plus higher utilisation following rig moves and this higher ARPOR should indeed see a very strong H2, but they have to start delivering now.

Creightons (CRL.L) - Preliminary Results

So, this was slightly below what many of us were expecting, despite being revised down during the year:

Adjusted diluted earnings per share excluding exceptional items, was positive 1.42p (2023:1.05p).

But it's not that far away that this is a major disappointment. As others have pointed out before, it just means that this continues to look expensive compared to any near-term expectations. However, few are invested here for the short term, given the spread and illiquidity.

Bernard has finally been thanked! Perhaps he was writing Liz Truss-style letters claiming that he was just an innocent victim in all this.

We are not a big fan of this presentation:

Net cash on hand (cash and cash equivalents less short-term element of obligations under finance leases and borrowings) is positive £2.2m (2023: negative £1.2m).

It is largely meaningless, and you have to scroll through the whole of the narrative to find the real position in the accounts. Which is actually a small net cash position of around £0.3m, excluding lease liabilities. Of course, there is likely to be some window dressing, and poor trading will have released working capital, but still, this is good news and what investors want to know.

The resumption of dividends is also good news, even if it is relatively small. The market seems to like the signal here, and the shares have recovered well. Not so much for the presence of any material good news but the lack of any further bad news. Although with many UK investors, their love of dividends is so great you can’t rule them out paying 5p more on the price to receive a 0.45p dividend!

This is still a high-risk stock as there is no discussion of how the current year has started or any outlook statement, although the dividend clearly signals that they are no longer in financial distress, and that is good news.

Eco Animal Health (EAH.L) - Final Results

The headline here is adjusted EBITDA ahead, but the actual growth seems rather pedestrian:

Adjusted EBITDA increased to £8.0m (2023: £7.2m)

Adjusted EBITDA is not profits, of course.

Earnings per share 1.55p (2023: 1.49p)

So these appear to have, at best, kept up with inflation. This is good news:

Net cash at the end of the period £22.4m (2023: £21.7m), reinforcing the Group's strong balance sheet with 36% of cash held outside China (2023: 19%)

But net cash should be considered the £8m outside of Chine, not £22m, in our opinion. This is up from £4m, though.

Broker Equity Development are forecasting flat revenue and declining EPS. So investors shouldn’t really be paying more than about 6-7xearnings. This makes fair value probably between 12-15p. Which becomes 24p-27p if you include c.12p per share net cash outside of China. However when we check the share price it is a totally bonkers 127p. However, perhaps investors are using the Sum of Parts method of valuation:

15p - Earnings

12p - Cash

100p - Hope/Cute piglet picture on Annual Report & Brokers notes

Robert Walters (RWA.L) - Q2 Trading Update

Another set of crap figures here:

It is a global business, so not all UK election worries, although it is worth noting, the UK is the worst performer. Hope seems to spring eternal in the investors here, who always price in the cyclical bounce. Sadly, this means that there is never an opportunity to buy this business cheaply enough to outweigh the risks of the unknown timing of the bounce back.

What they do know is that bounce back will be gradual and Partridge-like:

Our near-term planning now assumes that any material improvement in confidence levels will be gradual, and likely not occur before 2025. In this environment, we remain focused on being positioned to deliver the best outcomes for our clients and candidates, whilst maintaining tight cost discipline. These actions do not fully offset the first-half fee income reduction, but they position us well going into the second half of the year.

Recruiters sacking staff is perhaps the ultimate irony of an economic downturn!

Sosander (SOS.L) - Full Year Results

Sosander have managed to enhance margins, but at the cost of sales:

· Net revenue growth of 9.0% to £46.3m (FY23: £42.5m)

· Improved gross margin of 57.6% (FY23: 56.2%) (H2 FY24: 59.6%)

This is part of their shift away from growth towards profitability and away from online to opening physical stores. However, they are still loss-making but now ex-growth, which kind of asks the question - why bother?

Loss of £0.3m for FY24 following an upswing in PBT in H2 to £1.0m (H1 loss of £1.3m)

They also give us a Q1 update:

Post-period Trading (Q1 FY25)

Continued focus on prioritising margin enhancement and profitability

80% reduction in price promotional activity on Sosandar.com vs the same quarter last year

670bps improvement in gross margin to 63.4% (Q1 FY24: 56.7%)

Substantial positive swing from (£0.8m) pre-tax loss in Q1 FY24 to (£0.2m) pre-tax loss in Q1 FY25

Net revenue of £8.2m (Q1 FY24: £11.4m) reflecting prioritisation of increasing gross margins to improve profitability

It may be tempting to think that with such a large increase in gross margin they must have significantly improved the product. However, 60%+ isn’t out of line with what Quiz have, and the change appears to be driven by how they account for 3rd party sales:

The largest increase in administrative expenses is from third party commissions (increased by 43% on the prior year) which reflects the growth in revenue through our concession partners (notably NEXT & Marks and Spencer).

So a shift from COS to Admin Expenses explains why they still aren’t profitable despite the increasing gross margin. Losses have been offset by reduced inventory and they say there is further possibility of further reduction generating cash. However, this is not going to last forever.

Balance sheet remains robust with cash position remaining flat at £8.3m as at 30 June 2024 vs. 31 March 2024, allowing us to self-fund the planned store roll out

With £8.3m cash, they can keep this going for some time, but should they?Probably not, as our experience with another also-ran omnichannel fashion retailer Quiz demonstrates. As Quiz was a few years ago, Sosander is asset rich - £17.2m of net tangible assets are mainly cash and inventory. There are £0.6m of lease liabilities that you’d want to take off, but there’s an argument to be made that this would be a buy on assets at the £10m market cap level.

However, the current market cap is around £25m, so it would require a 60% fall from here to look interesting. And we’ve been here before, claiming that a cash-rich omnichannel retailer was a buy on asset value. And we got that one very wrong.

That’s it for this week. Have a great weekend!