Small Caps Live Weekly Summary

Welcome to our first weekly small caps life summary email!

For those of you who missed it, we did our first Small Caps Life more in-depth article yesterday.

Unfortunately, the informational advantage that we thought we would be conveying to subscribers rapidly vanished on Wednesday afternoon as the company, finnCap, produced an unscheduled trading statement confirming much of what we had deduced.

Sorry about that. Hopefully, in the absence of an updated brokers note it give investors a rough idea of where the figures may end up.

Still, we must have been convincing, since the Chairman & CEO of finnCap subsequently bought 130k shares each at 30.5p yesterday in response to our article. [This is a joke for the avoidance of doubt, they clearly have a much better view of the prospects of the business than us.]

Sam Smith only took her holding from 9.22% to 9.29% yesterday, but the Chairman's buy was his first since being appointed. There is a question of how much of the shares you want staff to own in a company like this. On the one hand, you definitely want interests to be aligned to avoid overpaying of staff. On the other hand, this company only has a free float of 20% already. Still, a buy is better than a sell.

As promised here is a summary of what we talked about on LCL/SCL this week. Click on our names for a direct link to that section on the SCL discord channel.

Large Caps Live 1st March

With the rise in the 10yr treasury in the US, Wayne took a look at the outlook for interest rates and inflation. Concluding:

(A) I think inflation is coming – indeed it has already been there in food prices in the UK according to our supermarket bills.

(B) But we will not know the real situation until lockdown ends – and the UK is months to years ahead of the rest of the world amongst major western economies.

(C) An increase in inflation does not mean an immediate increase in interest rates – there will be all sorts of political and economic considerations.

(D) Unemployment is the big issue but we do not know what the true rate is due to furlough and because we do not know how quickly retail will bounce back.

(E) We also have no idea what is going to happen to offices/shopping malls etc and hence employment.

(F) I think travel and leisure will be one of the first to bounce back.

(G) There are however a lot of small businesses that need major balance sheet repair.

(H) The Fed will slow down bond purchases before increasing rates.

Small Caps Live 3rd March

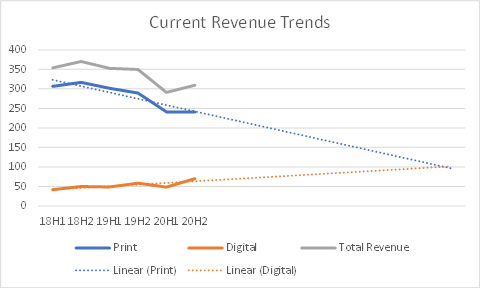

Reach (RCH.L) – Annual Results

Following Monday’s Annual Results, Mark didn’t see an obvious investment case here at these levels.

Either you have a £1.04bn business that generated about £95m FCF, so a 9% FCF yield. Or a 725m EV business generating 41m FCF or a 5.5% FCF. That range doesn’t look too expensive. But there are reasons I’m not rushing to invest here. Although the digital part of the business is growing well, the decline in print is rapid and print is still the vast majority of the revenue. The most important consideration versus other You can’t just split the businesses and value you them separately because the journalism of the print business is a key part of the digital business. You can’t say, for example, that digital is high-margin and print low margin – this is likely to be a false dichotomy. Investors here are buying a declining business, not two businesses one of which is growing rapidly.

It is also really hard to say how much the current trends are due to COVID-19 disruption. So there is a very large amount of uncertainty here. In summary, business could be cheap but also it is possible that the value to equity holders trends to zero over time.

If we take the current trends of the last few years it will be 4 and a half years before digital is that same size as print revenue, and it will still be only a £400m revenue business vs £600m today.

The other thing that makes me wary is this statement:

Customer registrations now at 5.8m (5.0m Dec 2020), more than halfway towards end 2022 target.

So, 10% of the UK population have registered as a customer. This means for digital revenue to equal 2020 print revenue 40% of the UK adult population would have to register as a customer. Anyone who has visited a Reach site without an adblocker knows that further monetisation of existing eyeballs would seem impossible/unwise.

Conclusion:

Fortune favours the brave when you were paying 50p/share. Buying above £2, however, requires a large amount of faith about the future trajectory of the business and I’m not sure that there are sufficient indications for a position of faith to be tenable, at least from these figures.

Microfocus (MCRO.L) – Commercial Agreement with Amazon Webservices

Leo viewed this announcement as lacking substance, compared with the c.15% rise in the share price that it caused.

MTI Wireless (MWE.L) - Final Results

Mark raised questions about the valuation here. With EBITDA flat for multiple quarters and trading on a 28x P/E, this looks potentially overvalued now.

Norcros (NXR.L) – Trading Update

Leo was pleasantly surprised by the progress the company is making.

So, in summary, I find the company considerably improved over the last year and I think this is one case where the recovery in the share price is justified.

Shanta Gold (SHG.L) - Final Results

Mark highlighted the risks of doing business in Tanzania.

So these do look good value but there is a risk that the Tanzanian government will take 50% of the economic benefit in time.

With the gold price having been weak this year there are plenty of gold miners who are now trading at low valuations, and without this risk overhanging them. My preference would be for one of those at current prices.

Small Caps Live 5th March

B&M Value Retail (BME.L) – Trading Update

Leo looked at this strongly performing retailer and the read-through to small cap supplier UP Global Sourcing.

Revolution Bars (RBG.L) – Interim Results Date

Leo looked at what may be delaying results here, concluding:

So I would say they are delaying their accounts because if they published them now they would not have enough liquidity to continue as a going concern over the next 12 months.

Goldplat (GDP.L) – Interim Results

Mark highlighted a particularly cheap valuation here, although not without its risks:

Although the lower gold price may mean H2 doesn't deliver as high an EPS as 1.45p it will still look pretty cheap when the share price is 7p.

Crystal Amber (CRS.L) – Management Commentary

Finally, this week Leo pointed out the particularly acerbic commentary from Crystal Amber towards Hurricane Energy.

Mark pointed out that perhaps the problem is that, although So Crystal Amber are a major shareholder, they are a minor stakeholder in Hurricane and it is not clear they have realised that yet!

Have a great weekend all.